First Industrial Realty Trust (FR) Faces Activist Pressure from Land & Buildings as Investor Urges Vote Against Directors Over Governance and $2B Valuation Gap

VOTE AGAINST DOMINSKI AND HACKETT

TO HELP UNLOCK $2 BILLION OF TRAPPED SHAREHOLDER VALUE AT FIRST INDUSTRIAL

Dear fellow First Industrial Shareholders,

Land & Buildings Investment Management, LLC (“Land & Buildings,” “L&B” or “we”), a significant shareholder of First Industrial Realty Trust, Inc. (NYSE: FR) (“First Industrial,” “FR” or the “Company”), is writing to you to highlight why we believe urgent change is needed at the Company to maximize shareholder value.

Over the past several months, we have publicly detailed our deep concerns about FR’s persistent undervaluation and the governance failures that we believe are directly responsible for this discount. We have issued three public letters and a detailed presentation laying out the facts and path forward.

The FR Board of Directors’ (the “Board”) response to each has been uniform and troubling: entrench, deflect, and protect the status quo. Shareholders deserve better. They deserve a Board that treats the $2 billion of trapped value as the emergency it is, not an inconvenience to be spun away.

Instead of heeding shareholder concerns, the Board continues to do the bare minimum, as exemplified by the Company’s recent announcement of share repurchases and a new director who seems to be more of the same

for FR. These defensive actions are simply too little, too late.

As shareholders, we have a critical opportunity to make our voices heard at First Industrial’s upcoming 2026 annual meeting of shareholders (the “2026 Annual Meeting”).

We intend to vote AGAINST the re-election of Chairman Matthew Dominski and Director H. Patrick Hackett, Jr. at the 2026 Annual Meeting and we strongly encourage all shareholders to do the same.

Mr. Dominski and Mr. Hackett Are Costing Shareholders $2 Billion

The governance failures at FR overseen by this Board are costing shareholders approximately $15 per share, or ~$2 billion in foregone market capitalization.1 As the longest-tenured directors holding key leadership positions on the Board, we believe that Mr. Dominski and Mr. Hackett bear direct responsibility for this outcome and that shareholders should vote against their continued service on the Board:

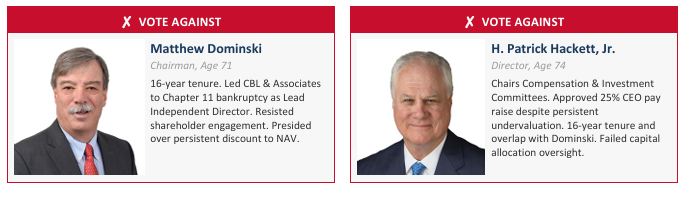

Matthew Dominski, Chairman (71 years old; member of Compensation, Investment, and Nominating/Corporate Governance Committees)2️⃣

• Questionable Independence: Mr. Dominski’s 16-year tenure on the Board raises serious questions about his independence and whether his continued service is in the best interests of shareholders.

• Concerning Judgment: We also question his judgment given his role as long-serving Lead Independent Director of CBL & Associates, a company that underwent Chapter 11 bankruptcy in 2020.

• Persistent Underperformance Under His Leadership: As Chairman, he has presided over FR’s persistent discount to NAV and a valuation gap relative to its closest peers that has deprived shareholders of billions of dollars in value.

• Resistance to Shareholder Engagement: When we initially attempted to engage with the Company on governance improvements, Mr. Dominski effectively threatened to discontinue communications with us if we did not immediately withdraw our director nomination.

Rather than address the Company’s failures, Mr. Dominski has chosen to deflect shareholder concerns and take reactive measures. We believe this pattern of behavior, suppressing dissent rather than confronting the status quo, is precisely why change in Board leadership is necessary.

H. Patrick Hackett, Jr., Director (74 years old; Chair of Compensation and Investment Committees)3️⃣

• Questionable Independence: Mr. Hackett has served alongside Mr. Dominski on the FR Board for 16 years, chairs two key committees on which Mr. Dominski also serves, and maintains a long-standing relationship with him as a fellow Chicago native. They also worked at JMB Realty, along with director Denise Olsen, at the same time. This raises concerns about his ability to provide truly independent and

objective oversight.

• Approval of Misaligned Executive Pay: As Chair of the Compensation Committee, Mr. Hackett led approval of the 25% increase in CEO compensation to $8.3 million in 2025 despite FR’s persistent undervaluation.

•Failed Capital Allocation Oversight: As Chair of the Investment Committee, Mr. Hackett has overseen a capital allocation strategy that has failed to close the discount to NAV.

We struggle to identify a single committee Mr. Hackett leads where results have been acceptable to shareholders.

We believe the insular, entrenchment-oriented culture on this Board is the single greatest obstacle to closing the valuation gap. It is not the portfolio. It is not the markets. It is the governance. Removing Mr. Dominski and Mr. Hackett from the Board is a critical step for First Industrial to achieve its full potential.

Persistent Valuation Discount and Poor Performance Against FR’s Own Peer Group

The Board and management’s failure to address FR’s valuation discount has resulted in meaningful total shareholder return underperformance. Measured against the Company’s own proxy compensation peers, the very companies the Board’s Compensation Committee selected to benchmark management pay, FR has underperformed by 17% over the trailing four-year period and 4% over the trailing three-year period.

These are meaningful shortfalls against the very peer group selected by the Board’s Compensation Committee. Yet management has received peer-level compensation for disappointing results. CEO Peter Baccile’s total compensation rose by 25% in 2025 to $8.3 million. The Board, with an average tenure of approximately 10 years,4 failed to add a single new director for five years and only moved to do so this week following our public engagement. A vacancy created by a director’s passing remained unfilled for nearly a year, yet the Board was resistant to adding experienced candidates proposed by Land & Buildings.

Let that sink in. The FR Board:

• Until this week, failed to refresh itself despite a vacancy created by the passing of a director nearly a

year ago and did not add a single new director for five years,

• Has overseen persistent undervaluation that has left roughly ~$2 billion in shareholder value on the

table,

• Yet rewarded FR’s CEO with a 25% pay raise.

In any other context, this would be considered a failure of oversight. At First Industrial, it appears to be business as usual. This is the boardroom culture Mr. Dominski and Mr. Hackett have built and perpetuated.

Recent Actions are Too Little, Too Late

Following our public engagement, the Company has taken defensive, reactionary measures, including authorizing a share repurchase program and appointing a new director. These actions appear to be attempts to placate shareholders and fall woefully short of addressing the Board’s underlying governance issues. The

proposed new director, Frank E. Schmitz, is another Chicago native with longstanding ties to the real estate community, similar to several existing Board members, raising concerns about his independence and underscoring the lack of meaningful change. Notably, his appointment is set to begin on June 1, 2026, after the 2026 Annual Meeting at which shareholders will be voting on the election of directors, further calling into question the timing and intent of this decision. These actions reinforce our view that meaningful Board change is urgently needed.

This is Not a Portfolio Problem, it is a Governance-Driven Discount

First Industrial owns a high-quality institutional industrial warehouse portfolio that has been materially transformed over the past decade. Nearly 40% of the portfolio has been newly developed, and more than 40% of legacy assets have been disposed of. FR’s portfolio quality today rivals that of blue-chip peers Prologis (NYSE: PLD) and EastGroup (NYSE: EGP) across a variety of key metrics.

4Reflects average tenure prior to recent appointment of new director.

Yet the market does not reflect this reality. FR trades at a mid-6% implied cap rate on market rents, while PLD and EGP trade in the low 5% range, a valuation spread of over 100 basis points.5 Green Street’s applied (private market) cap rates for FR and its closest peers are approximately the same, confirming that the private market values these portfolios as comparable.

If FR’s implied cap rate compressed to levels consistent with its closest peers, we believe FR shares could trade approximately $15 higher, representing more than 20% upside and approximately $2 billion of foregone market capitalization.

This gap is not a real estate discount. We believe it is a governance discount. This view was further corroborated when Prologis CEO Dan Letter noted at the Citi 2026 Global Property CEO Conference that cap rates on market rents are in the 5%–5.25% range, underscoring the steep discount at which FR trades.

Every day this Board refuses to address the status quo and implement meaningful governance changes, shareholders will continue to bear the cost of its governance failures.

The $2 billion valuation gap is not abstract – it is real money being left on the table by directors who appear more concerned with preserving their Board seats than maximizing the value of your investment.

While the applied (private market) cap rate spread between FR and both PLD and EGP has collapsed over time, reflecting the convergence in portfolio quality, the implied (public market) spread remains stubbornly wide at approximately 100 basis points. The private market recognizes FR’s quality. The public market has not. This is the governance discount we are seeking to close.

Our Plan to Unlock Shareholder Value

The removal of Mr. Dominski and Mr. Hackett would set the stage for what we believe are clear actions to

close the NAV discount and maximize value for all shareholders:

✔ Publicly commit to a plan to close the NAV discount with specific milestones and timelines.

✔ Initiate a $500M–$1B asset disposition program with proceeds returned to shareholders.

✔ Schedule an investor day with property tours within 90 days.

✔ Authorize a formal exploration of strategic alternatives if the discount does not narrow within six

months.

Strategic Alternatives: A Potential Next Step

If this Board and management team cannot close FR’s persistent discount organically, we believe they must evaluate strategic alternatives, consistent with the Board’s fiduciary duty to act in the best interests of the Company and its shareholders. We believe FR’s portfolio would be highly sought after by multiple acquirers:

• Prologis has acquired three public industrial REITs since 2018 at approximately 15–30% premiums: DCT ($9B), Liberty Property ($13B), and Duke Realty ($26B). FR’s geographic overlap makes it a natural fit and would result in meaningful revenue and expense synergy opportunities driving earnings accretion for Prologis.

• Blackstone has taken numerous REITs private in recent years at 25–40% premiums, has $53 billion in real estate dry powder, maintains its largest real estate exposure in the industrial warehouse sector, and has previously held an approximately 4% stake in First Industrial.

5Based on Green Street and Land & Buildings estimates.

We believe a transaction at our estimated NAV of $73 per share would deliver more than a 20% premium for First Industrial shareholders and unlock the trapped value this Board and management are seemingly unwilling to address.6 The protective, entrenched, status-quo mentality that permeates this Company must change for First Industrial to realize its full potential.

We ask shareholders a simple question.

If this Board is:

• Not willing to aggressively sell assets,

• Not willing to return meaningful excess capital to shareholders,

• Not willing to hold an investor day,

• Not willing to proactively refresh the Board, and

• Not willing to seriously evaluate strategic alternatives,

Then what exactly is its plan to close the $2 billion valuation gap? We have asked the Board and we have received no credible answer.

As a result, Land & Buildings intends to vote AGAINST the re-election of both Mr. Dominski and Mr. Hackett at the 2026 Annual Meeting, and we strongly encourage shareholders to do the same.

The status quo at First Industrial is unacceptable. The decision to install a new director after the 2026 Annual Meeting – rather than put that individual before shareholders now – speaks volumes about this Board’s desire to control outcomes while avoiding basic accountability to its owners. The Board’s resistance to meaningful change and its entrenchment-oriented approach to governance leave us with no choice but to seek change through the annual meeting process by urging shareholders to vote against both Mr. Dominski and Mr. Hackett. Land & Buildings’ engagement with the Company has demonstrated that it can be more effective outside the boardroom and that a critical step in improving First Industrial is removing those directors we believe are responsible for the Board’s failures. As such, Land & Buildings has determined to withdraw its nomination of

Jonathan Litt for election at the 2026 Annual Meeting and is urging shareholders to make their voices heard that the status quo is not acceptable by voting against the re-election of Mr. Dominski and Mr. Hackett at the upcoming 2026 Annual Meeting.

We believe that board refreshment is the catalyst needed to close FR’s valuation gap and unlock the full potential of this high-quality portfolio for all shareholders.

We strongly believe that with the right governance, FR shares can trade to our estimated NAV of $73 per share, representing over 20% upside from current levels. The only thing standing between shareholders and this value is a Board that refuses to act. It is time for that to change.

Sincerely,

Jonathan Litt

Land & Buildings Investment Management, LLC

Source: https://landandbuildings.com/wp-content/uploads/2026/03/LandB-FR-Letter-3-20-26.pdf

Member discussion