First Industrial Realty Trust (FR) Targeted by Land & Buildings Activism Over Governance Failures and Persistent NAV Discount

Land & Buildings Issues Letter Detailing Why Change Is Needed at First Industrial

Realty Trust

Board Has Repeatedly Refused to Collaboratively Engage With Shareholders

Company Has Persistently Failed to Achieve Its Potential, Consistently Trading at a Discount to NAV and to Its Closest Peers

Urges the Board to Take Steps Immediately for FR to Maximize Value for All Shareholders

Discloses Nomination of Land & Buildings Founder and CIO as Director Candidate for Election to the Board at the FR 2026 AGM

The full text of the letter is below:

Dear fellow First Industrial Shareholders,

Our engagement with First Industrial since our public presentation in early December 2025 has revealed an insular boardroom culture focused on prioritizing entrenchment rather than maximizing shareholder value. At every turn, we have found that this Board of Directors (the “Board”), led by Chairman Matt Dominski, has chosen to protect the status quo at all costs. The Board intends to nominate two directors with more than 15 years of tenure based on our understanding, has left a vacancy from a director’s passing nearly a year ago unfilled, and has refused to engage collaboratively with us on adding directors respected by the investment community.

FR trades at a mid-6% implied cap rate on market rents, while its closest peers, Prologis (NYSE: PLD) and EastGroup (NYSE: EGP), trade in the low 5% range, a valuation spread of over 100 basis points.1 Our estimated NAV remains $73 per share, as set forth in more detail in our December 2025 presentation, representing ~20% additional upside to the current share price.

Management Has Failed to Deliver Value for Shareholders

The track record under this Board’s oversight is deeply disappointing. FR management's and the Board's actions have led shares of FR to trade at a persistent and consistent discount to NAV and at a significant discount to its closest peers.

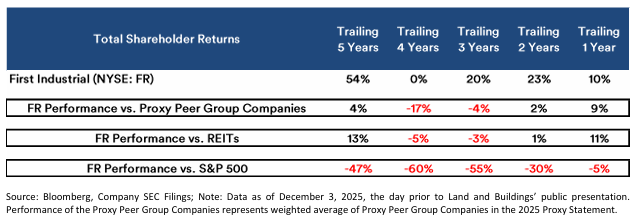

The table below compares FR’s total shareholder return to the Company’s own proxy compensation peers, the very companies the Board selected to benchmark management pay:

1 Bloomberg; Securities and Exchange Commission (“SEC”) filings.

FR has underperformed its proxy compensation peers by 17% over the trailing four-year period and 4% over the trailing three-year period. These are meaningful shortfalls against the very peer group selected by the Board’s Compensation Committee. Yet management continues to receive peer-level compensation for disappointing results. This is not a portfolio problem, FR’s same-store NOI and FFO growth have been comparable to Prologis and EastGroup. It is clear to us that FR’s underperformance is a governance and communication failure.

We strongly believe that a Board that has overseen this level of underperformance has no business resisting refreshment. Shockingly, no director has been added to the FR Board in the past five years. If the incumbent Board could not consistently deliver superior returns over 1, 2, 3, 4, and 5 years, why should shareholders trust them to realize the ~20% upside to NAV going forward and close the valuation

discount to its closest peers?

Steps to Generate Value

We urge the Board to take the following actions immediately:

• Publicly commit to a plan to close the NAV discount with specific milestones and timelines.

• Initiate a $500M–$1B asset disposition program with proceeds returned to shareholders.

• Schedule an investor day with property tours within 90 days.

• Authorize a formal exploration of strategic alternatives if the discount does not narrow within

six months.

• Immediately refresh the Board: Mr. Dominski and Mr. Hackett should not stand for re-election, and their seats, along with the vacancy created following Mr. Rau’s passing, must be filled with directors experienced in capital allocation and REIT value creation.

Constructive engagement requires a willing partner and to date, we have not found one in FR. Our preference would be to work together with FR to realize value for all shareholders. However, based on FR’s track record, we believe that we need to keep open all options available to us as shareholders – which is why Land & Buildings has nominated me, Jonathan Litt, as a director candidate for election to

the Board at the Company’s 2026 annual meeting of shareholders.

Sincerely,

Jonathan Litt

Land & Buildings Investment Management, LLC

Source: https://landandbuildings.com/wp-content/uploads/2026/02/LandB-FR-Press-Release-2-26-26.pdf

Member discussion