Medifast Inc. (MED) Targeted by Steamboat Capital Partners as Activist Flags Deep Undervaluation and Urges Cost-Cutting Turnaround

Letter to the Board of Directors of Medifast Inc.

Medifast Corporate Secretary

100 International Drive, 18th Floor

Baltimore, Maryland 21202

Dear Members of the Board of Directors,

Steamboat Capital Partners LLC (“Steamboat”) advises entities owning more than 5% of the shares outstanding of Medifast Inc. (“Medifast” or the “company”). We believe we are one of the three largest active investors in the company.

We appreciate having spoken and met with several members of the board over the past few weeks. As we expressed to the board, we believe that the company faces some significant challenges given the changes in the industry, but there is a credible path for an operational turnaround, and in that case the company’s stock is significantly undervalued. We believe that a newly initiated cost-efficiency effort could enable the company to regain its footing with sustainable profitable growth.

The public markets have lost faith in the current prospects of Medifast’s business strategy by valuing the company (with its current $105 million market cap, as of March 13, 2026) at $60 million less than its current cash balance ($167 million). While the company has been valued below its net cash since the beginning of 2025, the discount to its cash value has only increased, even as the portion of total assets represented by cash has increased and the proportionate amount of liabilities has decreased:

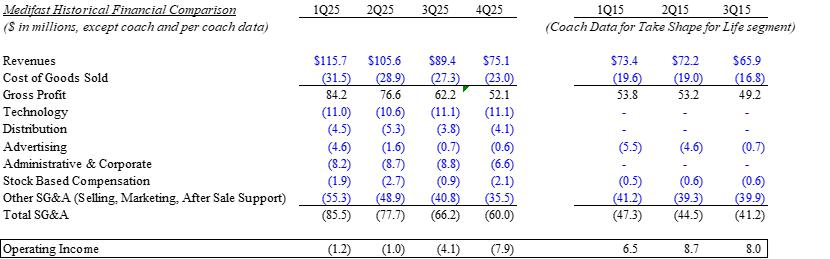

We believe that through thoughtful cost-cutting and right-sizing the business operations and corporate overhead, the company would be able to compete profitably even under the new realities of the direct-selling industry in a post-GLP-1 world. We believe that an emphasis on efficiency across technology, corporate and other areas would return the company to operational profitability. While we acknowledge that the company and industry have changed significantly over the past 10 years, we believe it is helpful to compare the cost structure of the company today with its Take Shape For Life segment in 2015 when the business was of roughly similar size to demonstrate the potential for corporate streamlining:

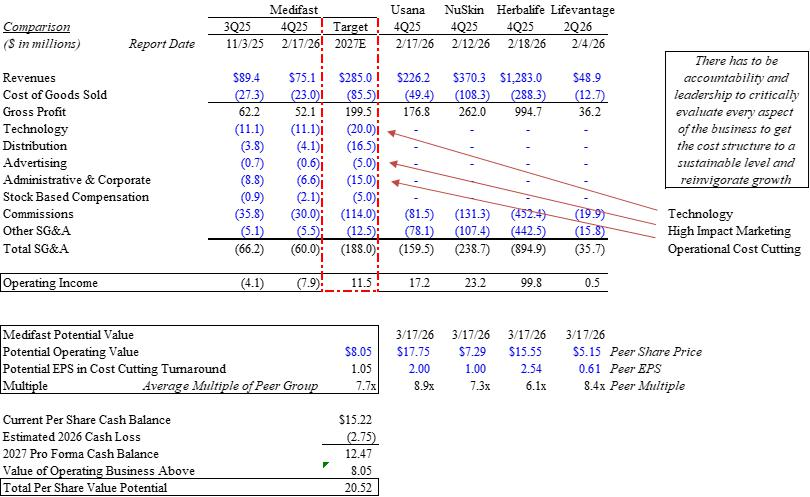

Likewise, we believe that a peer benchmarking exercise with other publicly traded companies in the direct-selling industry demonstrates that profitability is achievable, even with the competitive challenges from GLP-1’s and other industry pressures. While we acknowledge the difficult work ahead, we believe there is a credible path for Medifast to achieve a comparable operating margin as its peers. Even with very conservative valuation multiples on its operating business and inclusive of the cash losses required to achieve the turnaround, we believe that Medifast’s stock price could have substantial upside:

We look forward to the opportunity to work together with the board to successfully restore Medifast to profitability. In that light, we are happy to have further discussions about the matters raised in this letter.

Sincerely,

/s/ Parsa Kiai

Parsa Kiai

Managing Partner

Steamboat Capital Partners LLC

CC: Daniel Chard

Jeffrey Brown

Elizabeth Geary

Michael Hoer

Scott Schlackman

Andrea Thomas

Ming Xian

Source: https://www.sec.gov/Archives/edgar/data/910329/000121390026032212/ea028275401ex99-2.htm

Member discussion