OraSure Technologies (OSUR) Targeted by Altai Capital in Proxy Fight, Nominates Directors and Pushes Strategic Review Amid Performance and Governance Concerns

March 17, 2026

VIA EMAIL

Mr. John P. Kenny

Chairman of the Board

OraSure Technologies, Inc.

150 Webster St.

Bethlehem, PA 18015

CC: Board of Directors of OraSure

Dear Mr. Kenny and Members of the Board:

Altai Capital Management owns approximately 5% of OraSure Technologies, making us one of the Company’s largest shareholders.1 On December 17, 2025, we wrote to the Board stating our intention to nominate two candidates—John Bertrand, Co-Founder and former CEO of Digital Diagnostics, and myself, Rishi Bajaj, President and CIO of Altai Capital—for election at the 2026 Annual Meeting. Since that letter, Altai Capital has submitted formal nominations.2 We will be asking all shareholders to vote in favor of our nominees at the 2026 Annual Meeting. Please see Exhibits A and B, respectively, for my and Mr. Bertrand’s biographies.

Our case for change at OraSure rests on five pillars:

- Chronic Underperformance. OraSure’s share price has dramatically underperformed comparable companies and broader indices over both five- and ten-year periods. Recent underperformance has been driven by repeated operational and strategic failures under the current management team—failures that occurred on the Board’s watch. Despite this track record, the Company continues to burn cash pursuing speculative diagnostics investments to the detriment of shareholders.

- A Board Without Skin in the Game. Independent directors collectively own less than 1% of shares outstanding yet collect over $250,000 each per year in compensation. They bear little financial risk for decisions that have destroyed shareholder value. Shareholders who face the very real risk of losing money on their investment deserve a larger voice on the Board.

- Pay Without Performance. Over 90% of CEO Carrie Eglinton Manner’s compensation is not tied to share price performance. She has earned an estimated $15 million over her tenure while shareholders have lost 60% of their investment since 2023. Her incentives are plainly misaligned with shareholder interests.

- The Imperative for a Strategic Review. OraSure must evaluate a sale of the entire business alongside its current plan. We will represent and advocate for all shareholder interests in this process upon our appointment to the Board to ensure that the outcome delivers the best possible returns to shareholders.

- Nominees With a Track Record of Results. Rishi Bajaj led ContextLogic’s transformation from a company burning $80 million of cash per quarter to one that completed a $907.5 million acquisition, producing a share price increase of over 120%. John Bertrand built the company behind the first FDA-cleared autonomous AI diagnostic solution in healthcare. Both nominees will seek to align their compensation directly with shareholder returns.

The facts and events shown throughout this letter are clear. We present them so that shareholders can judge for themselves how OraSure arrived at this juncture.

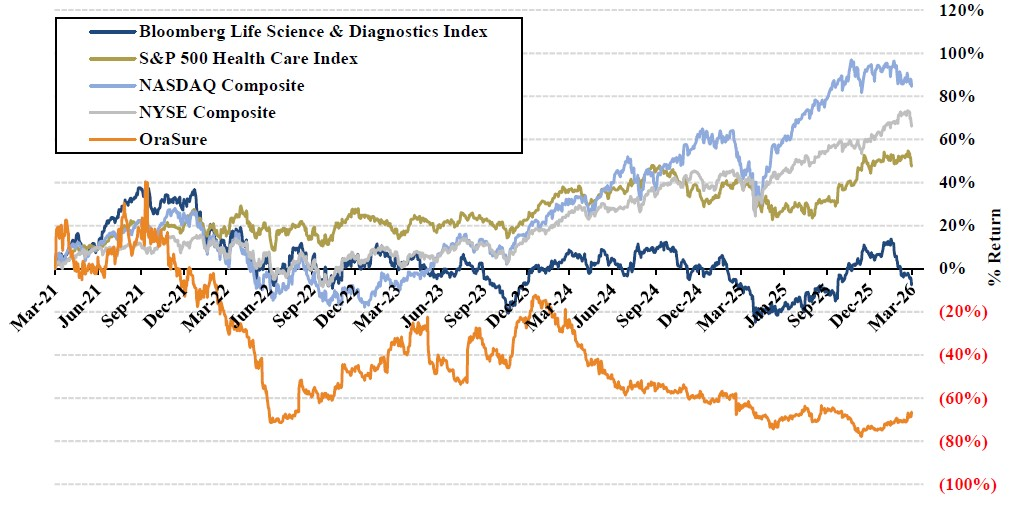

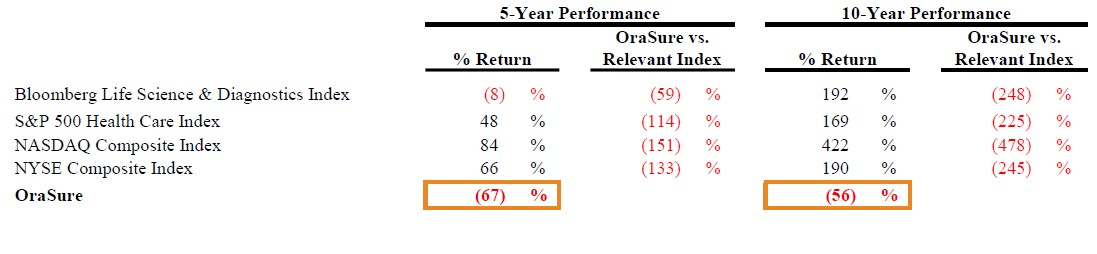

1. Chronic Underperformance

OraSure’s stock price is down 67% and 56% respectively on a 5-year and 10-year trailing basis. Over the past 5 years and 10 years, OraSure has dramatically underperformed its peers and the broader equity indices.

Most of the loss in value over the past two years was due to management failures under the Board’s watch. This is simply unacceptable and shareholders deserve answers and accountability.

Price Performance Graph: OraSure vs. Relevant Indices3

Price Performance: OraSure vs. Relevant Indices4

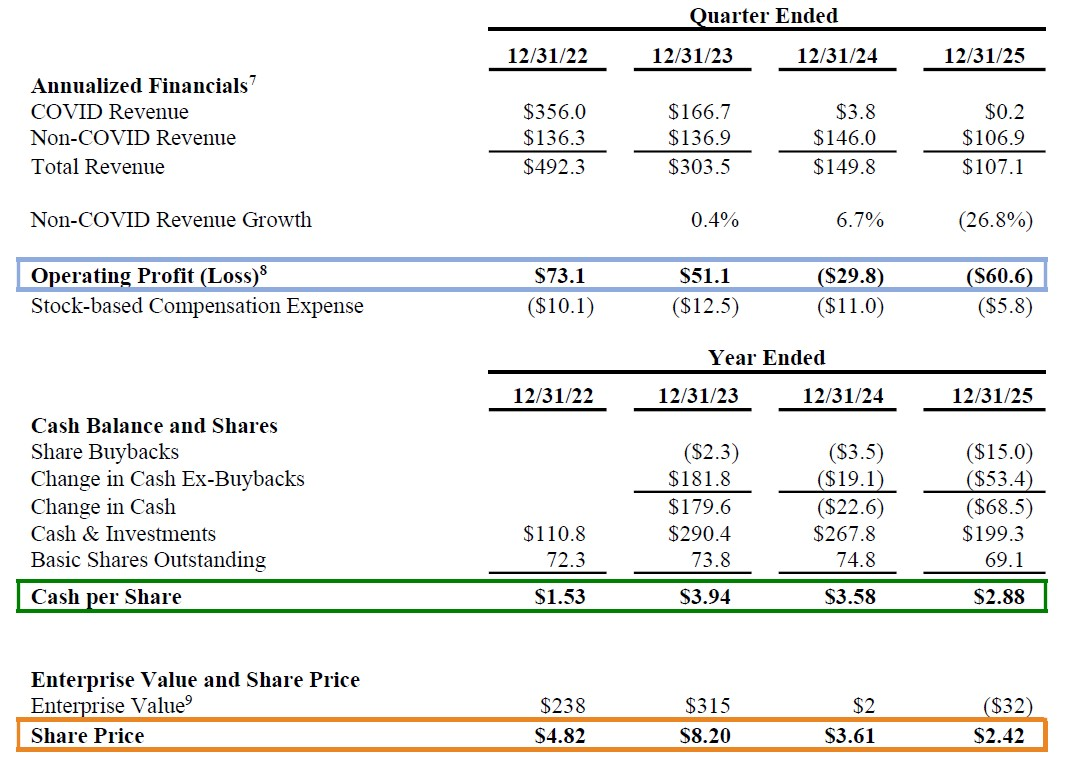

A $290 Million Question

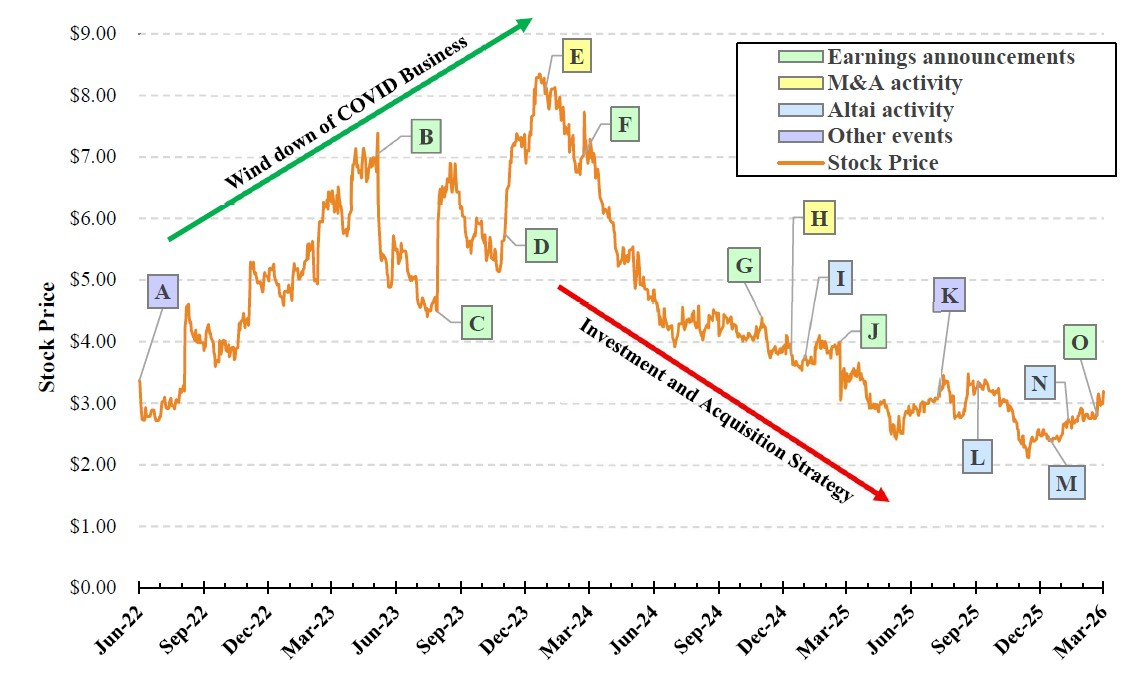

On June 4, 2022, Carrie Eglinton Manner became CEO of OraSure. At the close of 2022, OraSure had grown its cash balance from $111 million primarily by winding down its COVID testing business, collecting outstanding receivables, and selling remaining inventory. OraSure ended 2023 with $290 million of cash on its balance sheet ($3.94 per share) and its shares trading at $8.20.

This was an inflection point. The COVID windfall presented the Board with strategic choices. OraSure could have returned the cash to shareholders. It could have purchased established businesses with revenues and product volumes that could utilize OraSure’s excess manufacturing capacity. It could have pursued a sale of the business at a moment of financial strength. But instead, it chose to invest in speculative, subscale companies—and it invested poorly.

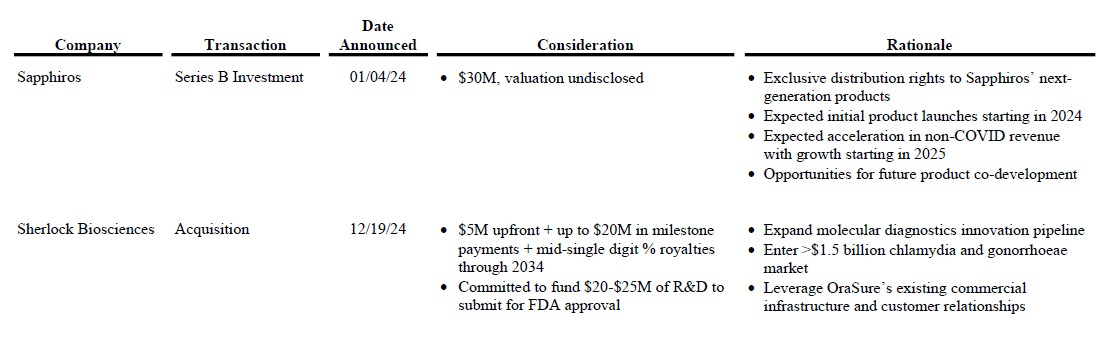

In January 2024, OraSure invested $30 million in Sapphiros, a startup diagnostic platform company with no commercial products on the market. The Company told investors that “distribution of Sapphiros’ products is expected to accelerate revenue growth in OraSure’s core business beginning in 2025.”5 That growth never came. By year-end 2025, OraSure’s core business (“non-COVID revenue”) had declined 27%, and the Company has not provided a recent update on the status of its Sapphiros investment or the revenue it was expected to generate.

Financial and Valuation Summary: 2022-20256

Doubling Down

By the end of 2024, cash had declined to $268 million and OraSure’s share price had dropped 56% over the year to

$3.61. In Q4 2024, the Company’s non-COVID business was generating annualized revenue of $146 million—essentially flat with Ms. Eglinton Manner’s first quarter as CEO—while losing approximately $7.5 million per quarter.10 A board focused on accountability would have paused and reassessed. This Board doubled down.

Prior to closing its 2024 fourth quarter, OraSure committed at least $25 million to acquire Sherlock Biosciences, an early-stage diagnostics company with no commercial products.11 The acquisition is troubling not only on its merits, but also because of the circumstances surrounding it.

Mara Aspinall joined the Board of OraSure in June 2017. On March 8, 2022, Illumina Ventures participated in an $80 million funding round for Sherlock Biosciences. On November 8, 2022, Ms. Aspinall became Chair of OraSure’s Board. On September 21, 2023, she became a Partner at Illumina Ventures. On December 19, 2024, OraSure, chaired by Ms. Aspinall, agreed to purchase Sherlock—a company backed by Ms. Aspinall’s own venture fund—for $5 million upfront plus the commitment to fund at least $20 million in R&D costs.12 The venture funds that had previously backed Sherlock, including Illumina Ventures, had themselves declined to invest further despite Sherlock purportedly targeting an estimated $1.5 billion growth market. OraSure stepped in where Sherlock’s existing investors would not.

The question of whether Ms. Aspinall’s dual role—as Board Chair of the buyer and as a Partner of an investor in the company being acquired—was properly disclosed and managed remains unanswered. The Company has not detailed Ms. Aspinall’s involvement in the acquisition process, nor confirmed whether she recused herself from the Board’s deliberations and vote related to the transaction. OraSure has also not explained why Sherlock, if its prospects were so compelling, was not marketed through a competitive sale process that could have attracted a buyer willing to pay more than $5 million upfront. These are important questions that require answers.

Altai Capital began conversations with OraSure regarding Board representation in November 2024. Tellingly, Ms. Aspinall resigned from the Board on October 28, 2025, after our ongoing discussions made clear that we would formally seek to have her replaced at the upcoming Annual Meeting if we could not reach an agreement. Five of the six Board members who approved the Sherlock acquisition, including Ms. Eglinton Manner, remain on the Board today. They continue to bear responsibility for their oversight (or lack thereof) in the Sherlock acquisition process and should be held accountable.

We note that Sherlock’s applications are currently under FDA review with the potential for approval in the first half of 2026. If elected, John Bertrand and I will evaluate Sherlock’s prospects with open minds. We would be delighted to change our assessment if the facts change for the better. But hope is not a strategy, and it is certainly not a reason to deny shareholders a voice on this Board.

Significant OraSure Strategic Transactions Since Ms. Carrie Eglinton Manner Became CEO

The Bill Comes Due

By year-end 2025, OraSure’s cash had diminished to $199 million ($2.88 per share)—a decline of over $90 million since the end of 2023. Non-COVID revenue had fallen to an annualized rate of $107 million, 27% below its 2024 run rate. Excluding approximately $5 million in share repurchases last quarter, cash is declining at roughly $12 million per quarter, driven by operating losses of approximately $15 million per quarter, which include $2–3 million in quarterly stock-based compensation.13 The trajectory is clear.

On the Company’s most recent earnings call, CFO Ken McGrath made a remarkable admission: OraSure is operating at approximately 30% manufacturing capacity. He stated that the Company does not expect to reach operating cash flow breakeven until 2027, “driven by our expected return to revenue growth, including contributions from our anticipated product launches.” Shareholders must endure at least another year of cash burn while hoping that Sherlock succeeds—a product that, as of today, has not received FDA approval and generates zero revenue.

This is the central strategic failure, and it deserves to be stated plainly. A company running at 30% capacity should acquire established businesses that can immediately absorb excess manufacturing capacity and improve profitability. Instead, OraSure pursued speculative, early-stage ventures with no near-term production volumes. Every dollar spent on companies that do not use OraSure’s existing infrastructure is a dollar that deepens, rather than addresses, the Company’s core problem. The true cost of these investments substantially exceeds their headline prices, and any future profit carries significant execution risk that investors should not be asked to underwrite indefinitely.

A change of strategy is warranted. We believe it is imperative for the Company to reduce its cash burn and safeguard itself against further misuses of cash, including additional value-destructive investments and acquisitions. Shareholder representation on the Board is critical to ensure that OraSure generates future value through more disciplined capital allocation or the sale of the entire business.

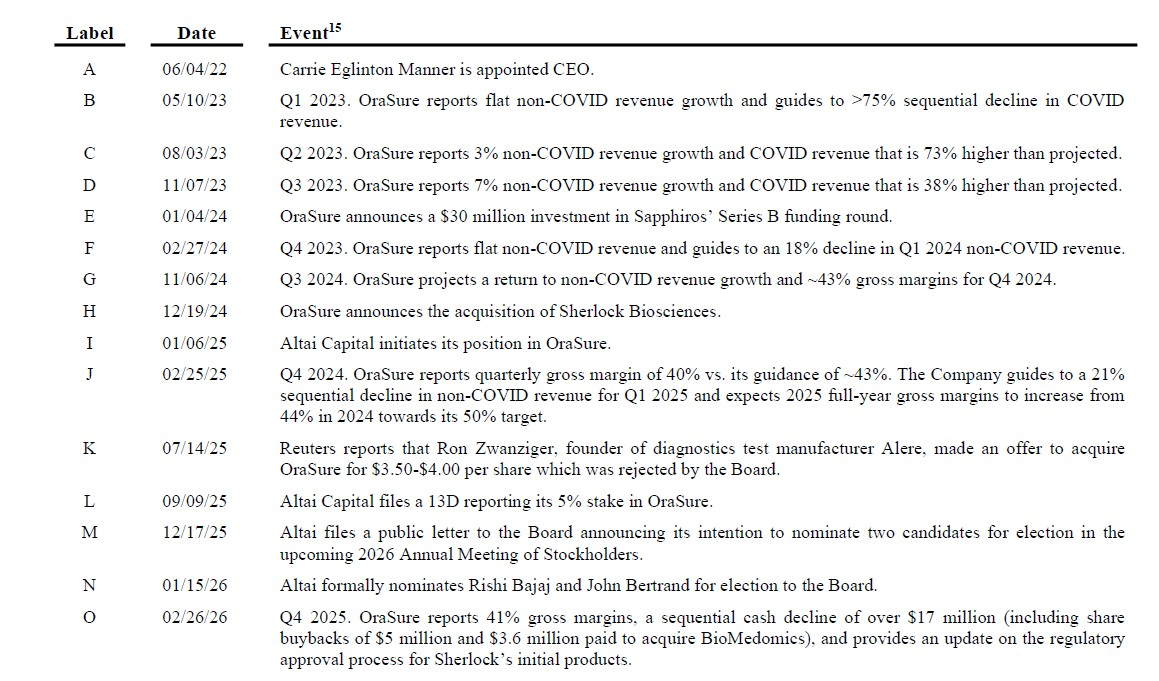

OraSure Share Price and Selected Events14

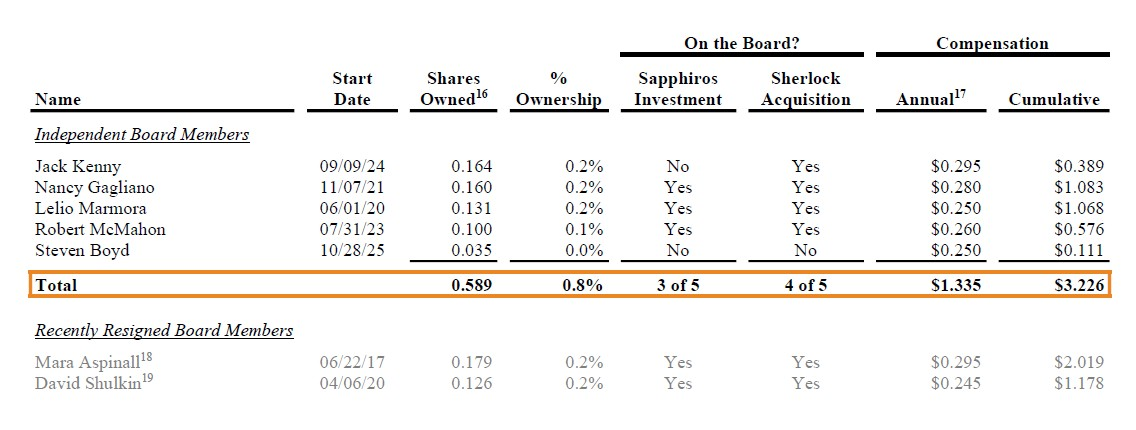

Board Ownership, Track Record and Compensation

Independent OraSure directors cumulatively own less than 1% of shares outstanding. Three of the five current independent directors oversaw the Sapphiros investment; four of the five were on the Board for the Sherlock acquisition. Together, these transactions are expected to cost shareholders over $55 million—not counting milestone and royalty payments or the additional operating losses attributable to underutilized manufacturing capacity. Unlike the shareholders they are supposed to represent, these directors bear virtually no financial risk for decisions that have destroyed value.

Despite this track record, the Board in 2025 increased its own annual stock-based awards by over 75%, from $105,000 to $185,000. Board members now earn annual compensation exceeding $250,000. Lelio Marmora and Nancy Gagliano have each earned over $1 million for their half-decade of service—a period during which shareholders have watched the value of their investment evaporate. The Board has been richly compensated for overseeing the destruction of shareholder value. That is not governance; it is a misalignment of interests that demands correction.

The contrast with Altai Capital is instructive. Altai owns approximately 5% of OraSure’s outstanding shares—more than six times the combined holdings of all five independent directors. Some directors may point to their relatively short tenure as an explanation for their low ownership, but that is precisely the point: the Board has neither sought nor required meaningful personal investment as a condition of service. Altai Capital has far more at stake in OraSure’s future than the directors who currently control it.

Board Ownership, Track Record and Compensation

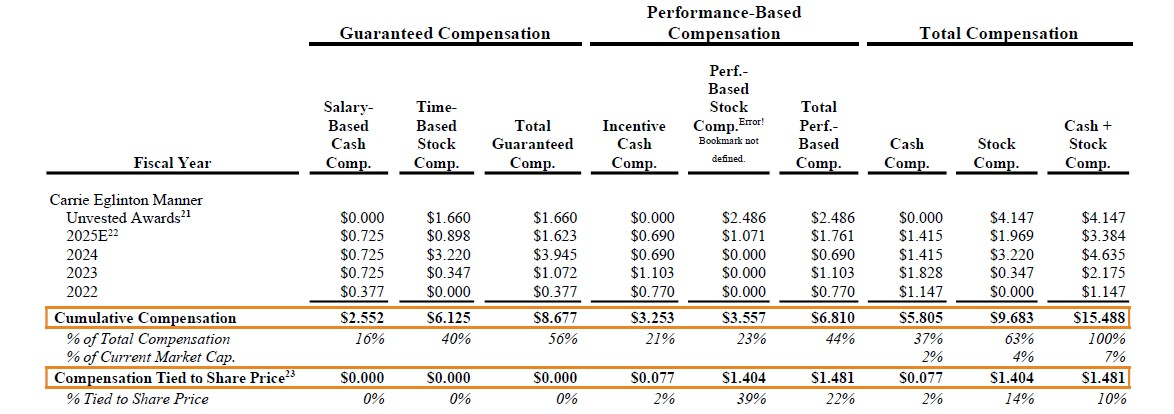

CEO Carrie Eglinton Manner’s Compensation20

When the COVID windfall left OraSure with $3.94 per share of cash at the end of 2023, the Board entrusted Ms. Eglinton Manner to deploy that capital wisely. Over her nearly four-year tenure as CEO, she is estimated to have earned more than $15 million in total compensation, including unvested awards, while investors who held OraSure shares since the close of 2023 have lost 60% of their investment. This is not an abstract governance concern—it is a concrete transfer of wealth from shareholders to management enabled by a Board that has refused to hold its CEO accountable.

CEO Carrie Eglinton Manner’s Compensation20

Ms. Eglinton Manner is incentivized to resist a sale: although a sale would deliver immediate value to shareholders, it would also end her roughly $4 million in annual compensation—most of which is guaranteed—representing 2% of OraSure’s market capitalization each year. The CEO’s economic interests are not aligned to the interests of the shareholders she serves.

The structure of this compensation is the wrong design for a company in OraSure’s position. Only 10% of Ms. Eglinton Manner’s cumulative compensation is linked to share price. The remaining 90% is paid through salary, time-based equity, and incentive bonuses tied to operating metrics—metrics that can, and did, pay out even as the stock declined 60%. Operating targets are inputs; share price is the outcome.

For a stable, growing business, this structure may appear reasonable. OraSure is not that company. It is burning cash, operating at 30% manufacturing capacity, and trading barely above the value of its cash balance. The central question facing shareholders is whether current management’s strategy will create equity value or further erode what remains.

We believe boards should pay extraordinary compensation only when management achieves extraordinary results. When this Board chose to support Ms. Eglinton Manner’s high-risk capital allocation strategy, it should have tethered the vast majority of her compensation directly to share price performance. It should have put her pay at risk. It did not.

One of the most fundamental responsibilities of any board is to hold executives accountable for poor performance. A board that understood the gravity of OraSure’s situation would have structured compensation to ensure that management bears real economic consequences if its strategy fails. This Board did the opposite. A CEO should not be handsomely rewarded for pursuing two questionable transactions while failing to drive either revenue growth or profitability. Upon our election, we will ensure that executive compensation at OraSure is restructured to align with shareholder returns.

4. The Imperative for a Strategic Review

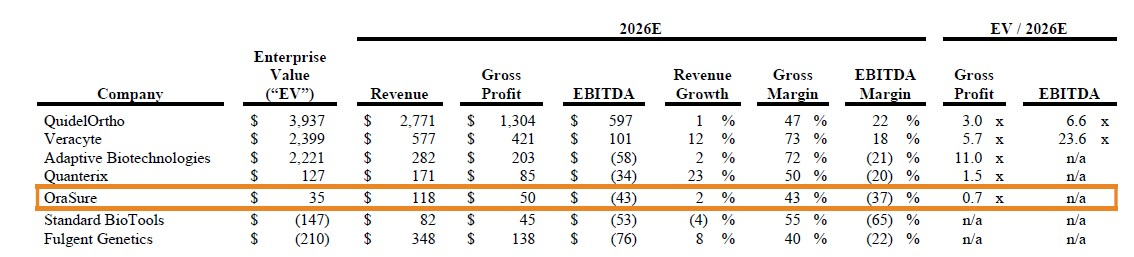

The diagnostics sector is a difficult market: competition is intense, pricing pressure is constant, products are often subject to unstable funding sources, and distribution requires significant ongoing investment. Scale matters enormously—the larger you are, the more efficiently you operate. Several smaller diagnostics companies similar in size to OraSure are valued at little to nothing by the market, in some cases below the value of their cash alone. If OraSure cannot grow revenue to a level that supports profitability, a meaningful recovery in its share price will be extremely difficult to achieve.

Comparable Company Analysis

Against this backdrop, OraSure faces three realistic paths: (i) grow revenue through organic investment and better use of its capacity, (ii) acquire established businesses at fair prices that bring additional volume, enabling the Company to rationalize costs and reach profitability, or (iii) sell the business to a larger acquirer that can provide the scale and distribution OraSure needs. Given the Company’s track record with options (i) and (ii), we believe option (iii) deserves serious and immediate evaluation.

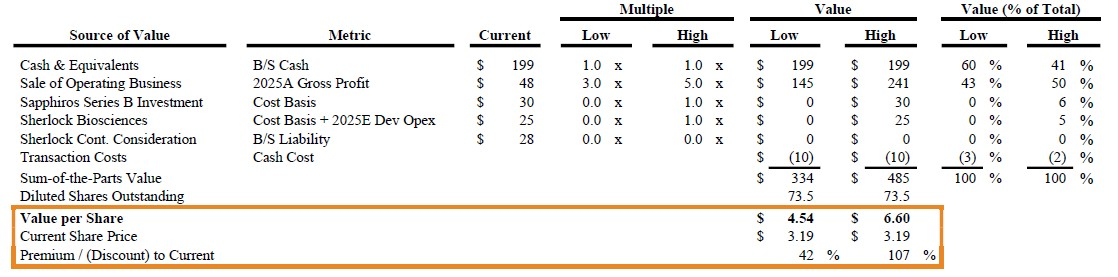

We believe OraSure is worth significantly more in a sale than as a standalone company. We value each component separately: the cash on its balance sheet, the current operating business, and the potential value of recent investments and acquisitions. At present, much of the value in OraSure’s share price simply reflects its cash balance. We believe the remaining operating business, including its underutilized manufacturing facility, could be worth between $145 million and $241 million to a strategic buyer. After deducting transaction costs (and valuing OraSure’s recent investments at cost in our “High” case), we estimate OraSure is worth $4.54 to $6.60 per share if sold—a 42% to 107% premium to today’s price. Through a competitive bidding process, especially if a buyer can underwrite significant synergies, these values could prove conservative.

Sum-of-the-Parts Valuation

As newly elected Board members, John Bertrand and I will seek to initiate a full strategic review that weighs the immediate value of an outright sale against the opportunities and risks in the Company’s current plan. A key concern is that the Board and management have an inherent incentive to preserve the status quo: they continue receiving generous compensation regardless of whether the share price falls, while shareholders bear the risk of further losses. Shareholders may prefer an immediate return of value without the threat of further capital impairment. That option deserves a fair evaluation, and we intend to ensure it receives one.

5. Nominees with a Track Record of Results

The best predictor of how a board member will serve shareholders is how they have served shareholders before.

In November 2023, I joined the board of ContextLogic which at the time was burning over $80 million of cash per quarter. After my appointment, ContextLogic sold its operating assets to Qoo10, a transaction that received overwhelming shareholder approval, and I was named ContextLogic’s CEO shortly thereafter in April 2024. As CEO, I significantly reduced the remaining expenses in the business, cutting cash burn to an insignificant amount.

In February 2025, I secured a $150 million strategic investment into ContextLogic from BC Partners, a well-known and highly-regarded investment firm founded in 1986 with over $40 billion of assets under management. Together, my colleagues at BC Partners and I, along with our excellent management team and board of directors, spent the next nine months continuing ContextLogic’s search for an acquisition target. On December 8, 2025, ContextLogic announced its acquisition of US Salt for $907.5 million, a transaction backstopped in part by newly committed capital from BC Partners, and I stepped down from my position as CEO. Following the announcement, ContextLogic’s shares closed at $8.10 per share, up over 120% from the low of $3.67 per share where its stock traded prior to my joining its board.24

Throughout my time as CEO, my compensation was (and is) directly tied to share price. The performance unit grants I will receive, which constitute the vast majority of my remuneration, require that ContextLogic’s share price reaches $10.00, $16.00, $21.00, and $30.00 per share over the next four years. My compensation package reflects our adherence to the bedrock principle of aligning management incentives with shareholder value creation. We believe this is the same model that OraSure’s Board should apply.

BC Partners has stated both publicly, and in private conversations with OraSure’s Board, that they are eager to work with me again—a testament to the results we achieved together. My fellow nominee, John Bertrand, is an extremely well-respected executive with a deeply relevant background in the diagnostics sector. Together, we offer OraSure’s shareholders something they do not currently have: Board members whose economic interests are genuinely aligned with their own.

Conclusion

After endeavoring to work constructively with OraSure—including numerous conversations with Board members and management over several months—the Board refused to appoint us. Our decision to formally nominate was a last resort, but one we welcome. We would have preferred collaboration; instead, we will make our case directly to the investors who own this Company.

Since Altai Capital announced our formal director nominations in January 2026, OraSure’s share price has increased 18%. Even taking into account OraSure’s recent commentary around Sherlock’s FDA application status, this appreciation should be surprising given the substantial operating losses reported in late February for their 2025 fourth quarter. We are not surprised. Investors are encouraged by the prospect of governance changes at OraSure. Many have reached out since our filing to express support for our pursuit of representation on OraSure’s Board and their enthusiasm for either a settlement or the opportunity to vote for our nominees at the Annual Meeting.

We urge the Company to listen to its shareholders and reach a fair settlement that results in the appointment of John Bertrand and me to the Board. If the Board chooses to proceed to a vote, we will continue to present our case to OraSure shareholders and seek to win our appointment through election at the Annual Meeting.

Sincerely,

Rishi Bajaj

President & Chief Investment Officer

Source: https://www.sec.gov/Archives/edgar/data/1116463/000090266426001649/p26-0793exhibit99.htm

Member discussion