Neuronetics, Inc.

3222 Phoenixville Pike

Malvern, PA 19355

Attention: Board of Directors

Dear Members of the Board:

We write as the largest independent shareholder of Neuronetics, Inc. ("STIM" or the "Company"), holding 14.12% of outstanding shares. We are long-term, fundamental investors with more than 20 years of operating experience in healthcare technology and over 15 years of multi-asset, multi-strategy investment experience. We firmly believe in the future of STIM's two business units. Both are

experiencing growing adoption and benefiting from a powerful secular shift. Patients of all ages are increasingly seeking durable, non-pharmacological, and clinically-proven solutions for depression and other mental health challenges.

We are entering into a generational inflection point in mental health treatment, and STIM’s businesses are uniquely well-positioned to take advantage of this new environment. The TMS unit possesses arguably unrivaled competitive advantages (technology, IP, data and scale). The clinic business, anchored by the Greenbrook platform, is poised to capitalize on the convergence of TMS, esketamine (Spravato), and the anticipated approval of psychedelic therapeutics.

Despite this potential, the Company has chronically underperformed. The root cause, in our view, is structural: a micro-cap company with finite capital and limited management bandwidth cannot adequately serve two distinct businesses simultaneously. As a result, shareholders who recognize STIM’s market-leading assets continue to suffer.

Massive Valuation Disconnect

Despite two highly-attractive and well-positioned businesses, the anticipated synergies of combining TMS and Greenbrook have not materialized. Since the December 2024 acquisition, pure-play peers on both sides have dramatically outperformed STIM while shareholders have suffered significant value destruction.

As we have previously communicated to management and the Board, we believe there is a clear solution and that a sale of the TMS business would unlock substantial shareholder value.

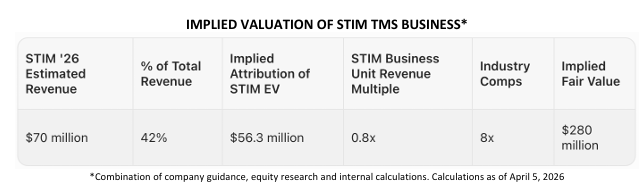

• TMS comps: Brainsway (BWAY) trades at approximately 8.4x forward revenue (~$560M EV on ~$67M projected revenue1)

• STIM's TMS unit is projected to generate ~$70M in 2026 revenue. Even applying a conservative 4x revenue multiple – a >50% discount to BWAY – implies $280M of value for the TMS unit alone2

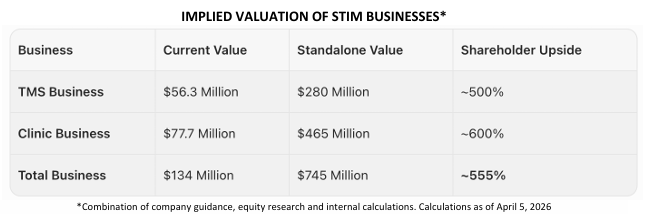

• STIM's entire enterprise value, encapsulating BOTH of its businesses is only ~$134M, a stark illustration of the discount to which it trades

Further, the sale of TMS would leave STIM with needed capacity to focus resources on its larger, faster growing clinic business, which is itself profoundly undervalued. Greenbrook is a world-class asset, and its trajectory will only strengthen as regulatory catalysts materialize, including the highly anticipated approval of Compass Pathways (CMPS) and other psychedelic therapeutics.

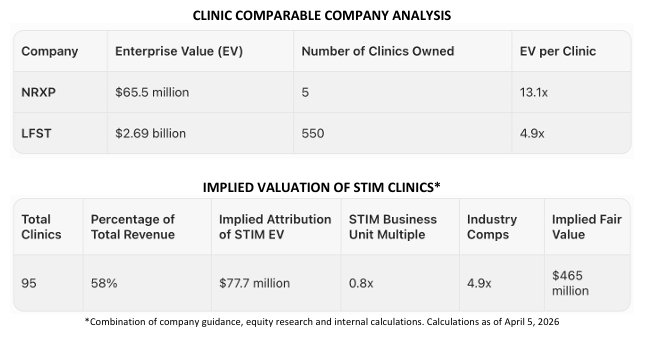

• Clinic comps: NRX Pharma (NRXP), operating just 5 mental health clinics alongside a pharma asset, trades at ~13x EV per clinic

• LifeStance Health (LFST), with 550 clinics where over 90% of revenue is derived from lower-growth, lower-margin traditional psychiatry, trades at ~4.9x EV per clinic

• STIM's Greenbrook platform, with 95 clinics exclusively focused on the higher-growth, higher margin modalities of TMS, esketamine, and emerging psychedelic therapeutics, could warrant a comparable multiple. Applying LFST's 4.9x to 95 clinics implies ~$465M of value for STIM, which doesn’t even factor in TMS

2Combination of STIM Company guidance, equity research and internal calculations

What a TMS Sale Would Enable

A sale of the TMS business, even when considering conservative levels, would deliver significant and immediate value to shareholders (at multiples of STIM’s current trading price). Critically, a transaction would also generate transformative financial flexibility, enabling management to focus resources on continuing to scale the clinic platform – a single, high-conviction business. Among other benefits, a sale would allow the Company to:

1 Generate a special dividend approximating the Company's current market capitalization (~$1.50- $1.75 /share)

2 Retire all outstanding debt and establish a clean balance sheet

3 Establish pro forma cash on the balance sheet of more than $100M

4 Provide capital and operational flexibility to pursue organic growth, greenfield expansion, and clinic acquisitions

The Upside for Shareholders is Immense

STIM is trading at severely depressed valuations when considering the market position and opportunity of its assets. When accounting for the conservative projections outlined above, we see 500% to 600% upside for STIM shareholders if the TMS business were to be successfully sold and the clinic business were to receive the resources and focus it needs to grow.

The Window of Opportunity is NOW – STIM Needs to Explore Alternatives Immediately While we have valued our open dialogue with management and the Board, STIM cannot afford to stall any longer and risk missing this extraordinary opportunity to monetize its attractive assets and reposition the Company as an industry leading clinical business at the forefront of a mental health treatment revolution.

We call on the Board to act with urgency and decisiveness: engage qualified investment bankers (we are happy to make introductions), and immediately initiate a formal, comprehensive process to evaluate strategic alternatives, including a sale of the TMS business.

STIM is simply too small to resource two structurally distinct businesses effectively. Expecting new CEO Dan Reuvers to grow both the TMS and clinic businesses is precisely the wrong strategic posture.

The far more compelling path is to monetize a highly attractive asset and empower Dan and the management team, fortified by a strong balance sheet and leading market position, to build the preeminent mental health clinic platform in the country.

The window of opportunity is now. A depressed market cap inhibits operational flexibility and limits the realization of growth opportunities. Every day of inaction compounds the risk and cost to shareholders, and further jeopardizes the Company's ability to realize the significant value of its assets and capture the upside of a generational inflection point in mental health treatment.

We look forward to working with you around the commencement and execution of the necessary actions for the benefit of all shareholders ahead of the annual meeting.

Sincerely,

Jorey Chernett

Pointillist Family Office

Source: https://www.sec.gov/Archives/edgar/data/1227636/000092189526000945/ex1to13da114528stim_040726.pdf