April 28, 2026

Dynatrace, Inc.

280 Congress Street, 11th Floor

Boston, Massachusetts 02210

Attn: Rick McConnell, Chief Executive Officer

Jim Benson, Chief Financial Officer and Treasurer Board of Directors

Dear Rick, Jim, and Members of the Board,

As you know, Starboard Value LP (together with its affiliates, “Starboard” or “we”) is one of the largest shareholders of Dynatrace, Inc. (“Dynatrace,” “DT,” or the “Company”). We appreciate the time you have spent with us and look forward to a continued constructive engagement.

Starboard has made a substantial investment in Dynatrace because we believe the Company is a high-quality, durable observability platform with a long runway for continued growth and an opportunity for significant margin expansion. We also believe the Company has significant strategic value as observability becomes more important in an AI-enabled world and the convergence of observability and security continues. In the recent software sell-off, it appears the market has ascribed significant near-term risk to Dynatrace. However, in our view, this perception does not appropriately reflect the reality of Dynatrace’s durable and differentiated platform, its strong competitive positioning, or the growing importance of observability as enterprise AI adoption accelerates. We believe these factors make Dynatrace more important moving forward, not less. In fact, enterprise adoption of AI should ultimately result in accelerating revenue growth

for Dynatrace. At the same time, we believe Dynatrace has opportunities to meaningfully improve operating efficiency, driving higher profitability and cash flow, while returning significant capital to shareholders. In sum, we believe Dynatrace has an opportunity for significant value creation, and we look forward to working with management and the Board of Directors (the “Board”) towards this shared goal.

Dynatrace Is a Leading Observability Platform that Should Benefit from AI Adoption

Dynatrace is a leading observability player and the clear leader in Application Performance Monitoring, the largest category within the observability market. Dynatrace’s end-to-end platform allows it to manage complex, heterogeneous environments spanning on-premise infrastructure, cloud environments, and both legacy and modern applications for its target large enterprise customer base. In these environments, reliability and integration are essential, and we believe

Dynatrace is well positioned to be an observability vendor of choice for years to come.

The Company’s consumption-based pricing model further strengthens this positioning and helps insulate the business from the risk of declining software seat counts as AI usage inside large enterprises increases. While many software vendors are still adapting their pricing models to better align with usage, Dynatrace benefits from already having a business model tied to customer

activity and the value it delivers. We see additional upside from continued adoption of the Dynatrace Platform Subscription (“DPS”) model, which has grown to represent 70% of ARR since its launch in 2022. As customers add workloads and consolidate their observability environments, Dynatrace should be able to continue to increase wallet share, strengthen customer relationships, and gain market share from legacy vendors. Management recently noted that DPS customers’ consumption growth is double that of non-DPS customers, and we believe the continuing shift towards DPS should provide a tailwind to net retention rates and, over time, revenue growth.

More broadly, from an industry standpoint, we believe the rapid expansion of enterprise AI workloads will increase the need for observability solutions. Today, the adoption of AI agents remains nascent, with recent industry reports indicating fully scaled deployments at less than 5% of enterprises1, suggesting a significant growth runway for end-to-end observability platforms like Dynatrace as penetration increases. As enterprises deploy more applications and more AI agents, the volume and complexity of telemetry data will grow materially. This growth should increase the value of platforms like Dynatrace that can ingest and interpret data across the full stack, particularly in large-scale, heterogeneous enterprise environments where reliability, trust, and actionable insights are of paramount importance.

Looking forward, we believe the next major step in observability will be enabling more automated and autonomous remediation through the deployment of AI agents. The ability to move from detection to diagnosis to intelligent action, safely and at scale, should increasingly differentiate leading platforms. We believe Dynatrace is well positioned in this evolution with its Davis AI engine, a tool that has been a part of the Dynatrace platform for nearly a decade and reflects the

Company’s meaningful and sustained investment in applying AI to observability workflows. Combined with Dynatrace’s strong incumbent position, we believe the Company is well positioned to help customers adopt more automated, AI-enabled operations over time.

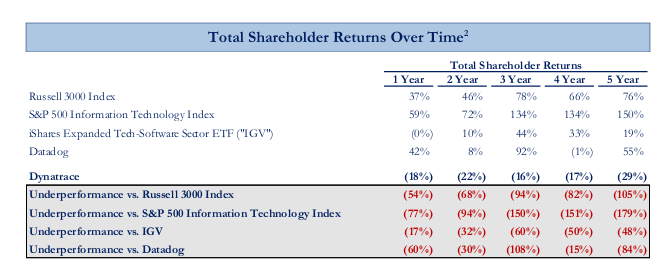

Despite Its Strong Positioning, Dynatrace Has Underperformed

Despite the tailwinds supporting the observability sector and Dynatrace’s attractive position within this market, the Company’s share price performance has been disappointing. As shown below, Dynatrace has significantly underperformed the broader market, a broad-based technology index, the software sector, and its closest public peer, Datadog, over the last 1, 2, 3, 4, and 5 years2. It is important to note that this underperformance predates concerns around AI disruption

of the software industry and that Dynatrace has also underperformed other similarly exposed software companies during this recent period of uncertainty.

1McKinsey: The state of AI in 2025: Agents, innovation, and transformation (November 2025).

2Source: Bloomberg, Capital IQ, Public company filings. Market data as of April 24, 2026.

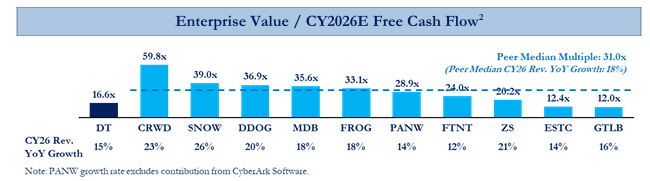

Beyond share price performance, Dynatrace also trades at a steep valuation discount to infrastructure software and cybersecurity peers. In fact, as shown below, despite revenue growth near the median of this group, Dynatrace is valued at nearly half the median multiple of the peer group. In our view, this discount does not reflect the quality of the Company’s platform, its strong competitive position, or its relevance to critical enterprise needs in an AI-first world.

We believe the Company’s poor share price performance and valuation discount to peers are a result of slowing growth, a lack of operating leverage, and investor skepticism regarding improved business performance in the near-to-medium term. We believe these factors are addressable and, as outlined below, Dynatrace has a tremendous opportunity for value creation.

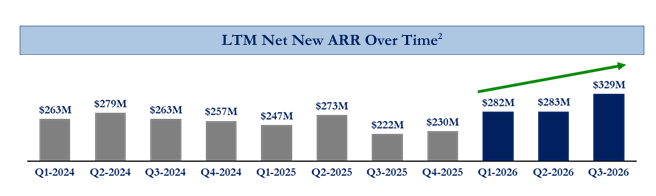

Dynatrace Has an Opportunity to Accelerate Revenue Growth

Following a period of exceptional growth, Dynatrace’s revenue growth has decelerated in recent years during a more challenged demand environment for software and as the business gained significant scale. However, we do not believe this deceleration will continue and view recent KPI trends as early evidence of an eventual return to accelerating growth rates.

As shown below, in recent quarters, net new ARR, a key leading indicator of revenue growth, has grown at a double-digit rate for three consecutive quarters.

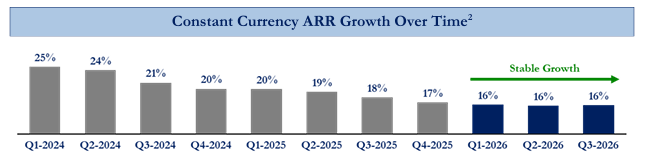

In addition, ARR growth has stabilized in the mid-teens on a constant currency basis over the last three quarters, and if Dynatrace meets its guidance for Q4 FY2026, the business will have generated 16% constant currency ARR growth for each of the last four quarters.

Constant Currency ARR Growth Over Time2

Positively, management has also noted that underlying consumption growth has trended north of 20% for multiple quarters. Over time, we believe consumption growth and ARR growth should converge, as consumption growth should drive future expansion and larger customer contracts that will flow into revenue ratably.

These data points indicate improving business performance and are the building blocks for an eventual reacceleration of revenue growth. Furthermore, we believe this recent momentum should continue as Dynatrace continues to take share from legacy competitors and will have its first full instance of DPS cohort stacking as we enter FY2027, meaning there will be three DPS cohorts that will become concurrently eligible for annual commitment resets, providing a larger

base of customers whose consumption growth could translate into ARR uplift.

We are also encouraged by the recent momentum of Dynatrace’s Logs offering and its contribution to growth. We believe Logs is an important growth driver because the offering is increasingly becoming a core part of the observability stack, with customers seeking to analyze logs alongside traces, metrics, and events in a single platform. With a high-quality logs product now in market, Dynatrace should be able to continue gaining share in this market and offer more value to its

customers. Management recently disclosed that Logs exceeded $100 million of annualized consumption as of Q3 FY2026 and is on track to reach $250 million of ARR by the end of FY2027. If Dynatrace is able to achieve this target and simply maintain stable growth in its core business, we believe the Company is well positioned to see revenue growth accelerate meaningfully.

Furthermore, as AI adoption grows inside large enterprises, the demand for observability should rise in tandem, driven by the need to monitor more applications, workloads, agents, and increasingly complex environments. We would expect this trend to appear first in consumption metrics, followed by ARR, and, over time, in reported revenue.

Dynatrace Has an Opportunity to Drive Improved Profitability

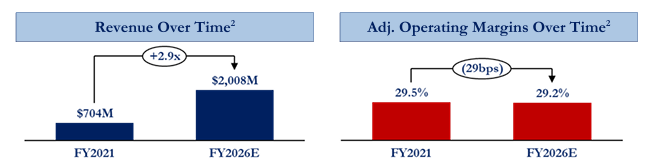

While Dynatrace has nearly tripled revenue over the last five years, adjusted operating margins have remained largely flat, as shown below. We believe the Company has an opportunity to meaningfully improve profitability going forward.

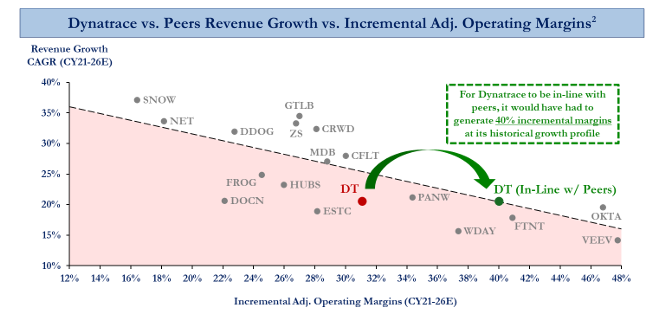

Over this period, Dynatrace’s incremental adjusted operating margins trailed peers growing at comparable rates, as shown below. Dynatrace’s incremental margins over the last 5 years have been just above 30% despite gross margins above peer levels, while peers of similar scale and growth profiles have produced incremental margins of approximately 40%. If Dynatrace had achieved peer median incremental margins during this time, its Adjusted Operating margins today

would be over 700bps higher than current levels.

Looking forward, we believe higher incremental margins can and should be a core driver of meaningfully improved profitability at Dynatrace. While consensus estimates suggest incremental margins will remain subpar over the coming years, we believe Dynatrace should be able to generate at least 40% incremental margins on future revenue growth. If it is able to do so, while meeting consensus expectations for revenue growth (which do not embed an acceleration), Dynatrace should be able to improve margins by approximately 350bps by FY2029, prior to any discrete cost reductions. We believe additional margin upside exists if Dynatrace can execute upon cost reduction opportunities across the Company’s key cost centers. Taken together, we believe Dynatrace should target at least 500bps of adjusted operating margin expansion by FY2029.

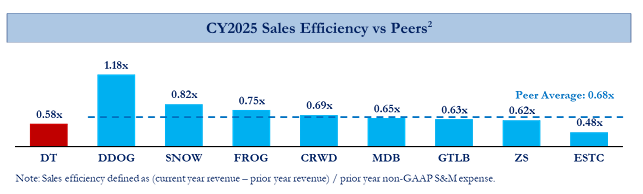

We believe the most significant opportunity to drive margin improvement lies in the Sales & Marketing (“S&M”) organization. Dynatrace’s sales efficiency has declined consistently over the last five years and compares poorly vs. peers, as shown below. This commonly used metric provides insight into how efficiently sales and marketing spend generates incremental revenue in the following year. If Dynatrace’s sales efficiency were in-line with the peer average, we estimate

the Company could either meaningfully increase revenue growth at current levels of spend or reduce S&M costs by approximately $75 million per year while maintaining the current growth rate.

Our diligence indicates that this inefficiency has been driven by both a headcount structure that has grown ahead of the business and declines in sales rep productivity due to a suboptimal go-to market motion. Despite nearly tripling revenue over the last five years, Dynatrace's S&M expense as a percentage of revenue has barely declined, suggesting that the Company has not achieved the

operating leverage that a business of this scale and growth profile should deliver. This is particularly true for a business with strong net retention rates. We believe these issues are addressable and represent clear opportunities to expand margins. While we are encouraged by recent changes management has made to improve the Company’s go-to-market function, our diligence indicates significant room for improvement remains.

We also believe Dynatrace has an opportunity to improve the efficiency of its Research & Development (“R&D”) organization. While we are encouraged by the recent momentum in the Logs offering, historically, product releases at Dynatrace have generally missed their targets for initial revenue milestones, suggesting the ROI on new product development has been, at best, mixed. While we agree that strong investment in product development is key to maintaining Dynatrace’s competitive positioning, we believe improved execution and greater discipline around R&D investment prioritization can meaningfully improve the efficiency of the R&D organization.

Moreover, recent advances in AI tools should be able to meaningfully improve productivity and lower costs across the organization, most notably in R&D and customer success.

In sum, we believe Dynatrace should be able to meaningfully improve the combination of its revenue growth + operating margins by delivering both higher growth rates and higher margins. We believe doing so will unlock significant shareholder value and solidify Dynatrace’s position as a leader in the observability market.

Dynatrace Has a Significant Capital Return Opportunity

Dynatrace also has an opportunity to create value by pairing the operational improvements outlined above with an aggressive capital return program. In the current market environment, high-quality software businesses such as Dynatrace are trading at severe discounts to intrinsic value, creating a rare opportunity to repurchase shares at valuation levels not seen in many years.

While the recent announcement of a new $1.0 billion share repurchase authorization is a step in the right direction, we believe the Company should execute this repurchase in the near-term and further commit to using a significant amount of its future free cash flow for ongoing share repurchases at these attractive valuation levels. Over the next three years, we believe Dynatrace

could repurchase more than $2.5 billion of its shares, which would represent approximately 25% of its current market capitalization, while still maintaining a significant net cash balance. By pairing a significant share count reduction with the operating improvements outlined above, we believe Dynatrace can significantly grow free cash flow per share, a key valuation metric, and drive meaningful value creation for shareholders.

The Ongoing Convergence of Observability and Cybersecurity

As AI advances, we believe the convergence of observability and cybersecurity will continue, as real-time visibility into application behavior, infrastructure anomalies, and data flows is foundational to both performance monitoring and threat detection. Dynatrace's deep telemetry capabilities and its ability to map dependencies across complex environments position it well to expand into adjacent security use cases over time, particularly as customers seek to consolidate

vendors and reduce the complexity of their monitoring and security stacks.

Furthermore, recent large-scale transactions in the observability and security sectors, such as Palo Alto Networks’ recent acquisition of Chronosphere and Cisco’s acquisition of Splunk, underscore the strategic importance of these capabilities and the significant value the market places on platforms that can operate at the intersection of these categories. In this context, we believe

Dynatrace possesses significant strategic optionality as a large pure-play observability vendor and would bring deep observability expertise to cybersecurity platforms. While we see clear opportunities for Dynatrace to improve both revenue growth and profitability, it is impossible to ignore the longer-term convergence of observability and cybersecurity, and the Board and management team must be open to all paths to maximize shareholder value.

Conclusion

In closing, we believe Dynatrace represents an extremely attractive investment opportunity. Dynatrace has been incorrectly bucketed as a company exposed to significant AI risks; however, we believe the business is well positioned to benefit from enterprise AI adoption. In our view, Dynatrace can deliver both a re-acceleration of revenue growth and meaningful margin expansion over the next few years while returning significant capital to shareholders. If Dynatrace can

execute on these opportunities, we believe Dynatrace can generate more than $3.30 of free cash flow per share by FY2029, nearly double FY2026 levels2. At the same time, we believe Dynatrace's strategic value is only growing, and the Board must be open to all avenues of value creation.

We are excited to be one of Dynatrace’s largest investors and believe the Company has a meaningful opportunity to create value through improvements in growth, profitability, capital allocation, and other strategic options.

We look forward to discussing these topics, among others, further with you.

Sincerely,

Peter A. Feld

Managing Member

Starboard Value