Starboard Value Urges Lamb Weston Holdings (LW) to Expand Cost Cuts and Review APAC Business in Strategic Letter

Lamb Weston Holdings, Inc.

599 S. Rivershore Lane

Eagle, Idaho, 83616

Attn: Mike Smith, Chief Executive Officer

CC:

Board of Directors

Dear Mike, We appreciate the time that you and the Lamb Weston team have spent with us over the past year. As we have discussed, we believe that Lamb Weston Holdings, Inc. (“Lamb Weston” or the “Company) is a high-quality business operating in a structurally attractive industry. We are encouraged by the meaningful progress made since the leadership transition, including improved pricing discipline, a clear volume inflection, and deliberate capacity curtailments that have begun to restore utilization toward normalized levels.

We believe the opportunity extends beyond the initial recovery. The return of volume growth and more rational capacity behavior are important milestones, but stabilization alone will not be sufficient to unlock Lamb Weston’s full earnings potential. In our view, the Company is well positioned to enter a new phase of value creation, one defined not only by normalization of industry conditions, but by a structural improvement in margins, capital allocation, and earnings power. Specifically, we believe you should expand the already announced cost reduction program and conduct a strategic review of certain international operations, particularly within Asia Pacific (“APAC”).

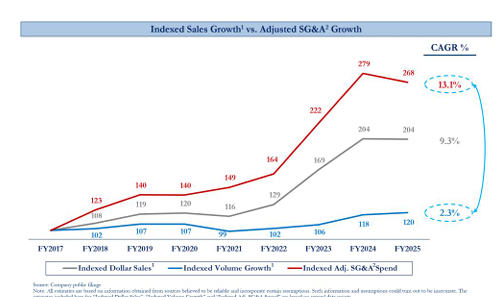

The Company has announced a cost reduction program targeting at least $250 million in annualized run-rate savings by the end of FY2028. While this is a welcome first step, it is important to recognize that the vast majority of the announced savings are expected to come from cost of sales, with comparatively limited impact on selling, general, and administrative expenses (“SG&A”) and overhead. We believe the larger opportunity moving forward lies within SG&A. As you see in the chart below, since IPO, Lamb Weston’s sales have roughly doubled, yet the Company has generated little to no operating leverage. Most of the Company’s revenue growth since IPO has been price-driven, as opposed to volume-driven. Therefore, we would expect Lamb Weston to have realized significant operating leverage. You have not. It is time to catch up.

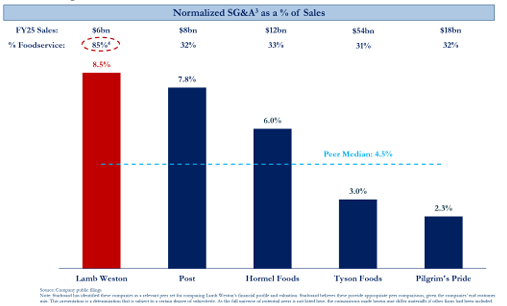

Lamb Weston’s annual SG&A burden relative to its revenue base now exceeds the median of its peer group. This is particularly striking given that Lamb Weston generates a significantly higher proportion of its revenue from foodservice than its peers, a channel that should inherently support a leaner go-to-market model and lower SG&A intensity, compared to its peers with greater exposure to branded products and retail sales.

We believe Lamb Weston should target approximately $500 million in total cost reductions, representing roughly $250 million of incremental savings beyond the currently announced program. Achieving this level of savings would bring Adjusted SG&A2 to approximately 4.5% of net sales, which we believe is more appropriate for the Company’s business model and customer mix. Notably, even at that level, Lamb Weston’s SG&A intensity would remain above that of certain foodservice-focused peers, including Tyson Foods and Pilgrim’s Pride.

In our view, a $500 million total cost reduction program is both achievable and necessary to ensure that margin expansion reflects not only improved industry conditions, but also durable structural discipline. To be clear, we do not want you to focus solely on targeting a cost savings number, as that often gets lost in reported results. We would like you to announce an Adjusted SG&A2 target of 4.5% of revenue and would like the board of directors (the “Board”) to focus and incentivize the 4.5% Adjusted SG&A2 target.

In addition to cost optimization, we believe the Board should undertake a focused strategic review of the Company’s international portfolio, particularly certain APAC operations. While international diversification has merit, portions of the APAC segment face increasing competitive pressure, which has weighed on overall profitability and added unnecessary distraction to the turnaround. We believe a deliberate assessment of these operations will sharpen capital allocation, improve consolidated margins, and unlock additional value. Importantly, our diligence suggests the Company’s APAC operations generate little in terms of earnings, but there would be considerable interest from local players should the Company seek to divest its operations.

We believe that expanded cost savings focused on SG&A opportunities, combined with a thoughtful divestiture of under-earning APAC operations, provide a clear path to restoring Lamb Weston’s EBITDA margins to 25%. Importantly, this level of profitability is not dependent on topline growth, but rather on the Company’s cost discipline and its ability to focus its portfolio around higher-return geographies. Therefore, we believe the Company should introduce a 25% EBITDA margin target as a medium-term goal, with the appropriate budgeting and incentives. Once again, a margin target, rather than a cost reduction target, provides greater transparency and accountability by allowing investors to easily track the Company’s progress over time through measurable profitability outcomes.

Mike, we greatly appreciate the hard work so far and are thrilled to be able to buy a substantial position at this valuation. We believe a valuation of 6.7x EV/ NTM EBITDA5, proforma for a 25% EBITDA margin, is extremely attractive, especially for a high-quality business in a stable and capacity-constrained industry. While we are pleased with the progress to date, we believe there is much more to be accomplished and are excited to be able to get involved at this valuation. We look forward to working with you and the Board as you focus on accomplishing and surpassing this margin target.

Lamb Weston remains a strong business with durable competitive advantages in a concentrated industry. We look forward to engaging constructively as the Company moves into this next phase of value creation and stand ready to support actions that strengthen Lamb Weston’s performance and long-term shareholder value.

Sincerely,

Jeffrey Smith

Managing Member

Starboard Value LP

Member discussion