Sturm, Ruger & Company (RGR) Targeted by Beretta Holding as Activist Pushes Board Change and Criticizes Governance Failures

Fellow Ruger Shareholders,

Beretta Holding S.A. (“Beretta Holding” or “we”) is the largest shareholder of Sturm, Ruger & Company, Inc. (NYSE: RGR) (“Ruger” or the “Company”), with a 9.95% ownership stake. We are writing to you because Ruger shareholders have endured years of value destruction, and urgent change is needed to restore the value of your investment.

We invested in Ruger because we believe in the strength of its iconic American brand, loyal customer base and meaningful assets. Instead of delivering strong returns to shareholders, the Company has produced persistent share price underperformance, disappointing financial results and governance failures that have insulated the Board of Directors (the “Board”) and management from accountability.

Beretta Holding brings a unique perspective – we have been manufacturing firearms for more than 500 years, successfully navigating industry cycles while building durable, profitable businesses grounded in disciplined leadership, innovation and operational excellence.

Years of Shareholder Value Destruction and Opportunity Cost Under the Current Board

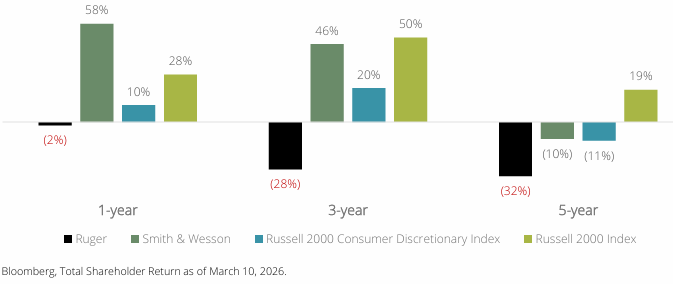

Ruger’s prolonged share price underperformance reflects a fundamental failure of oversight at the Board level. Despite operating in the same macroeconomic and regulatory environment as its peers – and during one of the most favorable demand environments in the Company’s history – Ruger has consistently trailed Smith & Wesson Brands Inc. (“Smith & Wesson”), its closest public peer, and the broader market, delivering disappointing returns to shareholders.1

Ruger Total Shareholder Return vs. Peers (Total Shareholder Return of Ruger, Smith & Wesson and the broader market)

This outcome is particularly troubling given Ruger’s strong brand recognition, loyal customer base and long standing position in the firearms industry. Companies with these attributes should be well positioned to generate durable shareholder returns across market cycles. Instead, Ruger’s shareholders have endured years of lost opportunity while the Company’s closest public peer, Smith & Wesson, and the broader market have delivered substantially stronger returns.

The Problem Isn’t the Market: It’s Ruger’s Execution

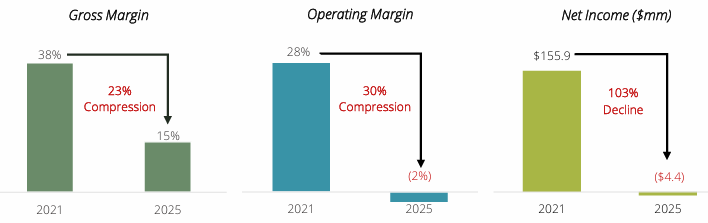

Ruger’s financial results show an alarming pattern of sustained operational deterioration, highlighted by a sharp and consistent decline in profitability – since 2021, gross margin is down 23%, operating margin is down 30% and net income is down 103%.

Margins and Net Income Have Cratered Under the Board and Management’s Watch2

This sustained margin erosion raises serious questions about management’s ability to control costs, maintain manufacturing efficiency and scale operations effectively. At the same time, Ruger has failed to pursue actionable opportunities in the market, leaving the company with significant strategic gaps.

X No meaningful exposure to the military and law enforcement channels

X Meager accessory offerings

X Ammunition, munitions and outdoor products are key missed opportunities

X De minimis international presence

X Underutilized brand

X Lackluster presence in the shotgun category

Weak Board Oversight Has Allowed Ruger’s Underperformance to Persist

Ruger’s years of underperformance happened on the watch of the same long-tenured directors who seemingly control the Board today. Do not be misled by the recent so-called “board refreshment.” We believe these directors still remain firmly in control, collectively representing more than 65 years of Board tenure and having overseen the period during which Ruger significantly lagged both its closest competitor and the broader market. These same directors own only about 1% of Ruger’s shares, giving them limited personal financial exposure to the Company’s performance. Instead of building meaningful ownership stakes alongside shareholders, the primary financial incentive keeping these directors in their seats appears to be their annual cash retainers. In our view, shareholders deserve a Board that is meaningfully invested in the Company’s success and accountable for its performance.

The Path Forward: Shareholder-Driven Change Is Needed to Reload Ruger

At the upcoming Annual Meeting, you will have the opportunity to elect four independent director candidates nominated by Beretta Holding. These nominees bring the skills and experience needed to help restore operational performance and strengthen oversight of management. They understand the firearms business

and the responsibility of a public company director to drive value for all shareholders.

Our independent nominees will serve all Ruger shareholders – not Beretta Holding. We are NOT seeking control.

As Ruger’s largest shareholder, our interests are aligned with yours – if we succeed you succeed. That is what we are here for.

We look forward to engaging directly with you in the coming weeks as we distribute our proxy materials and present the full case for change at Ruger.

Respectfully,

Beretta Holding S.A.

Source: https://www.sec.gov/Archives/edgar/data/95029/000092189526000740/ex991todfan14751002_031926.pdf

Member discussion