Dear Fellow WEX Shareholder,

Impactive first invested in WEX Inc. (“WEX” or the “Company”) in 2021 because we believed in the strength of the Company’s underlying businesses, its assets and the potential for WEX to significantly improve its performance. Today, as a 4.9% shareholder, we continue to believe the Company has tremendous runway to do better. However, it has become clear that significant change is needed at WEX to realize its full potential.

Impactive has a proven track record of working constructively with the companies in which we invest. We have only had to nominate directors one other time, and, in that instance, we reached a settlement before the annual meeting. But WEX has proven to be different. Over the course of our multi-year engagement, WEX has continuously done everything possible to avoid accountability to shareholders – while seemingly ignoring the fact that during this time its share price has been abysmal. Given the extraordinarily low support for three incumbent directors last year – including the CEO / Chair – we are apparently not alone in our frustration.

That is why we have nominated three uniquely qualified director candidates for election to the Board of Directors (the “Board”) at WEX’s 2026 Annual Meeting, which is scheduled to be held on May 5, 2026. We urge you to vote on the WHITE universal proxy card to elect our three candidates and pave the way for WEX to finally deliver for shareholders.

WEX has responded to our nominations by attempting to distract shareholders from its persistent underperformance. The Company has published a smokescreen of ad hominem attacks and red herrings while providing very little in the

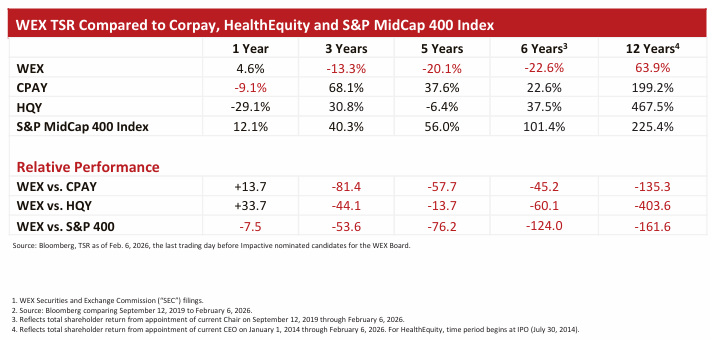

way of facts or data to substantiate its claim that the status quo is the best path forward. However, the numbers speak for themselves: in the past six years since the CEO has served as Chair, WEX shares have trailed primary Mobility competitor Corpay, Inc. (NYSE: CPAY) (“Corpay”) by 45%, primary Benefits competitor HealthEquity, Inc. (NASDAQ: HQY) (“HealthEquity”) by 60%, and the S&P MidCap 400 Index by 124%, as poor operating performance and capital allocation have collapsed its margins, returns on capital, and trading multiple. The Board has chosen to reward the CEO / Chair with $85 million in compensation over this period1, while WEX’s market capitalization has halved, falling by $3.4 billion.2 Shareholder performance has improved only over the last year following the launch of Impactive’s public campaign.

Poor Financial and Strategic Decisions Have Driven Underperformance and Undervaluation

WEX has performed poorly across numerous time periods and metrics, including the CEO’s 12-year tenure. Consider the following data points:

We believe this underperformance is the result of a series of bad decisions on the part of management and the Board, including:

Inferior operating execution in Mobility, WEX’s largest business. After years of subpar investments in innovation and acquisitions, WEX is growing 60% slower than Corpay with roughly half the operating margins, despite having started

with almost identical fleet assets ~10 years ago.5

• WEX Mobility Segment Economic EBIT margin trails Corpay’s Vehicle Payments segment by an astonishing 24 percentage points. This gap has persisted for at least five years and widened over time.6

• Despite lower margins and recent increases in sales, marketing, and “product innovation,” WEX’s Mobility segment has organically grown at only 2.7% annually over the past three years, compared with 6.7% at CPAY Vehicle Payments.7

• This underperformance is not explained by product mix, the freight recession, or geography; WEX’s organic growth has also trailed Corpay when isolating for the North American Fleet segment where they most directly compete.

Returns on capital that have trailed Corpay since the current CEO started, despite beginning with similar fleet assets. WEX’s return on invested capital8 declined from 15.8% in 2013, the year before Melissa Smith was appointed CEO, to 5.3% in 2021. The ROIC only improved to 8.3% by 2025 when the Company began purchasing shares, after being urged to do so by Impactive and other shareholders. We believe the following lapses have driven this underperformance:

• A culture of empire building and chasing growth via dilutive M&A, even with questionable strategic fit and deteriorating returns.

• A spectacularly failed Corporate Payments strategy, whereby the Board has repeatedly allocated shareholder capital towards the lowest quality Embedded Payments business and failed to successfully build out payables or cross border. WEX’s Corporate Payments segment revenue has declined over the last two years, dramatically missing the 10-15% management target set in 2022.

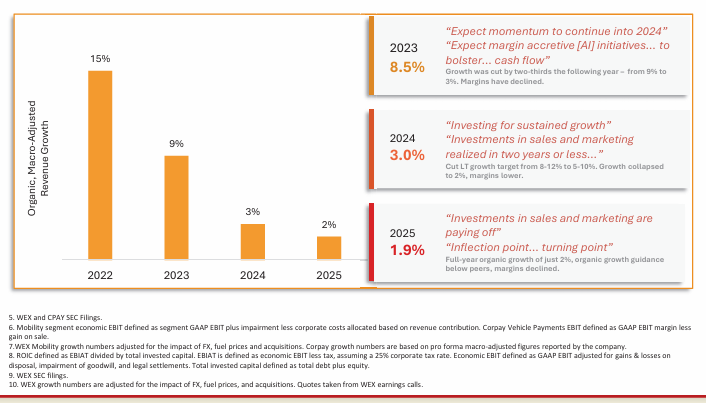

Quarter after quarter, year after year, management promises “momentum,” “growth acceleration,” and “investments driving inflection points,” while both growth and margins have declined:

Failure to proactively or seriously consider asset divestitures. Impactive has highlighted the embedded sum-of-the parts value at WEX repeatedly since 2022, including when valuations were much higher than they are today, and the

Board failed to act. How can we trust the current Board to proactively take advantage of value creation opportunities in the future when they have not in the past?

As a result of this underperformance on operations and capital allocation, Corpay’s EPS in 2025 was 77% higher than WEX’s, despite being 12% lower in 2013,11 the year before the current WEX CEO started.

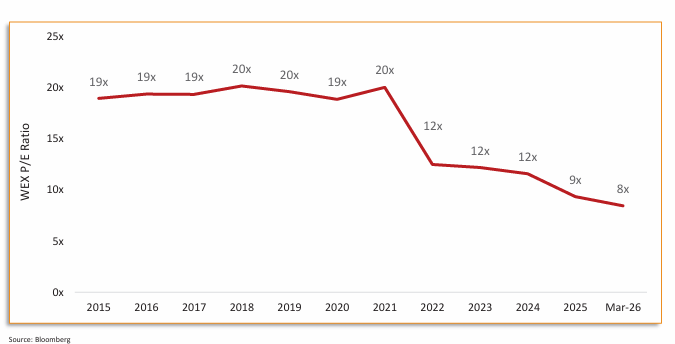

The decisions outlined above have eroded shareholders’ confidence and led to a valuation disconnect. At present, WEX is valued at the lowest point in its public history:

The Board has failed to hold management accountable for these missteps.

To the contrary, since combining the CEO and Chair role under Ms. Smith, WEX directors have rewarded her with $85 million. WEX’s CEO compensation has

consistently increased despite missing targets provided to investors, because the Board has set her compensation targets below the numbers publicly guided to investors and significantly increased the median market capitalization of

the comparable proxy peers relative to WEX’s own market capitalization.12

How can shareholders believe the Board, particularly the Leadership Development and Compensation Committee, will advocate for shareholder interests when

they pay management more and more for continuously delivering less and less?

The Board Has Rebuffed Shareholders’ Concerns and Has Continued to Entrench Itself

In the face of shareholder discontent and poor performance, the Board has not proactively enhanced its corporate governance or made proactive changes. Rather, it has sought to entrench itself even further, and only begrudgingly made adjustments when pressured publicly. Consider the following:

• The non-executive directors have limited exposure to the consequences of their decisions and seem to lack independence. Collectively, they own just 0.18% of WEX’s outstanding shares.13

• Despite the extraordinarily low support for certain directors at last year’s Annual Meeting – ranging from just 57% to 67% of the votes – the Board seems to have concluded that minimal change is warranted.

o There have been no strategic changes, no course correction of leadership, and no change in the business mix, while WEX’s margin and growth gap compared with its closest peer continues to grow.

o The Board only conducted a strategic review under duress after public embarrassment by Impactive – and no rationale was provided for its conclusion.

• The recent changes to the composition of the Board have been reactive and seemingly, at best, capricious or, at worst, improper manipulation of the Company’s corporate machinery.

o Only after Impactive filed its Schedule 13D amendment disclosing five potential Board nominees did WEX add one new Board member, David Foss, and announce its intention to reduce the size of the Board to 10 seats at the 2026 Annual Meeting.

o Then, in March 2026, the month after Impactive nominated four director candidates, WEX announced that it would now be further reducing the size of its Board to nine seats at the 2026 Annual Meeting.

• Further, the Board granted an extension of the mandatory retirement age to 75, allowing a 20-year entrenched lead independent director – Jack VanWoerkom – to remain on the Board.

Throughout all of this, WEX has been unable to provide a consistent rationale for refusing Impactive’s request for Board representation, even in light of the expressed support of other shareholders.

WEX’s Scorched Earth Defense

WEX's Board has demonstrated that it will deploy every available tool – including the attempted weaponization of state and federal banking regulators – to try to disenfranchise shareholders and insulate itself from shareholder accountability.

The Utah Department of Financial Institutions sent Impactive a letter inquiring whether our proxy solicitation may trigger banking change-in-control provisions – a legal interpretation that we believe has never been applied to any proxy contest at a public company that owns a Utah industrial bank. Impactive later received a letter from the San Francisco FDIC regional office – which interestingly, the Company had publicly disclosed as having already occurred, demonstrating that they were likely behind it.14 In the letter, the FDIC confirmed the customary proxy solicitation exemption under the federal Change in Bank Control Act (“CBCA”)15 and made certain general inquiries of Impactive.

To be clear, the CBCA specifically exempts customary proxy solicitations for matters to be considered at a shareholder meeting from the prior notification requirement, so long as the proxies terminate within a reasonable period after the

meeting. We are cooperating fully with the regulators to allay any concerns. Further, since responding to the inquiries, we have received no additional requests from either the FDIC or the Utah Department of Financial Institutions.

We believe WEX and its advisors have gone to great lengths as part of the Company’s concerted entrenchment strategy to create the appearance of regulatory risk where none exists. As the Company well knows, there is a clear exemption for customary annual proxy votes, and even if this exemption did not exist, Impactive’s 4.9% ownership is well below the 10% control threshold under federal or state law. Further, three nominees for a nine-seat Board represents a clear minority, particularly considering that only one of our three nominees has any affiliation with Impactive, and all, if elected, would serve as fiduciaries of WEX and all of its shareholders. Again, we want to be clear: there has been no indication to date that either the Utah Department of Financial Institutions or FDIC will require a change of control notice or application to be submitted by Impactive, and Impactive is confident in its position that no indicia of control is implicated by way of this proxy solicitation.

Ironically, WEX Bank has had a troubled history with FDIC enforcement actions and compliance and is currently subject to an FDIC enforcement measure. It is our understanding that it is rare to receive multiple FDIC consent orders in a three-year period. Of the 27 industrial loan company charter banks in the United States, WEX Bank is the only bank with more than one enforcement action including one under an active consent order now entering its 30th month. Our nominee Ellen Alemany has significant experience working constructively alongside regulators as a banking and payments CEO – we believe she would bring critical insights to the Board that would help engender a culture of compliance. Shareholders can be better served by a Board whose interactions with regulators are focused on solving

WEX Bank’s ongoing compliance issues and not sham attempts at disenfranchising shareholders, the true owners of the Company.

We plan to focus on the facts, the numbers and what matters to shareholders rather than engaging in low-road attacks. However, we must refute the most ridiculous ad hominem accusations contained in WEX’s recent communications

(please see Appendix).

Specifically, regarding the attempts to discredit Lauren Taylor Wolfe, we trust investors to see through the Company’s deliberate distortions of reality. As one chairman who served on a public board with Ms. Taylor Wolfe put it, “Lauren

was an exceptional board member who, along with her team at Impactive, helped guide us through a series of strategic and capital considerations, and see around corners in a very turbulent Covid market. She listened intently, synthesized

diverse viewpoints and was highly collegial in making her points… Lauren also had the insight to invest big on the Covid dip – she was bold and brilliant while the rest of the world sat on their hands.”

Jim Fox, the Chairman of the other public company board on which Ms. Taylor Wolfe served, found his experience working with Ms. Taylor Wolfe and Impactive so compelling that he asked to be included on the WEX slate – and was among our first nominees announced in October 2025.

Actionable Steps for Value Creation

We believe that WEX should take specific steps to reverse its trend of underperformance, improve growth and operating margins, and close its valuation gap. These include the following:

Close the gap in Mobility operating performance by implementing cost rationalization and pricing initiatives and evaluating why investments in sales & marketing, innovation and product velocity efforts have failed to drive profitable

growth. We believe our ideas can close 10-15 points of the 24-point gap to Corpay’s Vehicle Payments margins, which would drive a 30-40% increase to overall Adjusted EPS.

• Impactive solution: Our diligence suggests there is material margin upside via unexercised pricing, product segment gross profit levers, and a disciplined ROI lens on sales, marketing and innovation spending to drive efficiencies. Our

nominee Kurt Adams has an excellent track record of margin enhancement and asset integration in his former roles at Corpay and at United Health Optum, both direct competitors to WEX. No current Board members have any operating experience running the disparate businesses under the WEX umbrella – and it shows in the results.

Improve capital allocation and strategic alternatives by continuing to use excess cash to support share repurchases and instilling M&A discipline.

• Impactive solution: Nominees Ellen Alemany and Lauren Taylor Wolfe have deep experience in optimizing capital alternatives, pruning portfolios to prioritize profitability and evaluating a sum of the parts strategy to maximize shareholder returns.

Conduct strategic review of business portfolio with people actually incentivized to maximize shareholder value. This would include confirming that the synergies of keeping the business segments together create more value than could be achieved by separating non-core assets, evaluating return on capital and return on invested capital as standalone entities, analyzing why WEX has not been able to monetize its strategic industrial loan company bank asset, considering purchase price, trading multiples, management focus, and inorganic opportunities when conducting that review.

• Impactive solution:

o Replace the current Board Chair. Given consistent share sales, the CEO’s stock ownership today is less than 2x her annual compensation despite a 29-year tenure at the Company. She is therefore incentivized to maintain the status quo, as a bigger business has translated into more compensation.

o Ms. Taylor Wolfe, as the representative of a large shareholder, would bring an ownership perspective to the Board – something that has been missing since Warburg Pincus fully sold its position four years ago.

o Ms. Alemany has specific technical experience with banking and regulatory issues that is also lacking on the Board and necessary for the proper evaluation of strategic alternatives. Despite holding one of only 27 Industrial Bank Charters in the country, the WEX Board does not have a single Board member who has been

the CEO of a bank.

Shareholders Have a Critical Opportunity to Upgrade the Board

Impactive’s highly qualified nominees have the experience, expertise and ownership mentality necessary to help guide WEX forward. Following is an overview of the nominees’ experience and qualifications:

Kurt Adams: A technology and payments executive with over 25 years of experience leading and driving growth strategies for corporate payments and health benefits platforms across public companies and within a major financial

services organization, including WEX’s most direct competitors, US Bank Voyager, Corpay and United Health Optum. He would be the only Board member who has successfully led and operated identical businesses. Highlights include:

• Operational acumen at direct competitors has already been acknowledged by WEX’s Board, as he was their top choice to add as a director

• Former CEO of Optum Financial, a larger direct competitor to WEX’s Benefits business

• Independent of Impactive and has personally purchased shares of WEX

• WEX has acknowledged Ms. Alemany’s value to the Board

• Directly oversaw Corpay’s highly successful Corporate Payments strategy, including operations and capital allocation in cross-border and AP direct businesses

Ellen Alemany: A veteran financial services CEO with more than 35 years of banking and payments experience and deep expertise in governance, regulatory, strategy and operational execution from her numerous senior executive and board

roles. Highlights include:

• Banking and fintech executive, most recently as Chairwoman & CEO of CIT Group and board of First Citizens, that would bring the only bank and regulatory experience to WEX and will help to improve the Board’s culture and quality of governance

• Will be helpful in advising on the complexities of monetizing banking assets

• Independent of Impactive and has personally purchased shares of WEX

Lauren Taylor Wolfe: A long-term and significant shareholder representative with extensive experience in investment management, capital allocation and corporate governance. Highlights include:

• Has studied WEX’s business over five years of ownership, including exhaustive research with customers, former executives and fellow shareholders

• Brings prior board experience executing sum-of-the-parts strategies, operational improvements and margin expansion, and importantly, a shareholder perspective that is sorely missing

• Will help to restore shareholders’ confidence that their interests are prioritized in the Board’s deliberations and management accountability is enforced – nobody is more economically aligned with the best interests of all shareholders

We believe these director candidates would represent a meaningful improvement over the incumbent directors we are seeking to replace. Specifically, we urge shareholders not to vote for the re-election of Nancy Altobello, Melissa Smith,

and Stephen Smith for the following reasons:

Nancy Altobello

• Tenure TSR: -22.1% vs. +27.9% for CPAY; 5,000 bps deficit

• As Chair of the Nominating and Governance Committee, Nancy is responsible for allowing the CEO and Chair role to remain combined despite stark underperformance

• She also approved the extension of the mandatory retirement age from 72 to 75 to allow a 20-year Board veteran to remain in the Lead Director (and former Nom & Gov Chair) role

• She has stonewalled the prospect of having a large, long-term shareholder in the boardroom

• Her audit experience at Ernst & Young is redundant with other Board members’ skillset and minimally relevant compared to the banking, regulatory and payments expertise the Company needs, and Ellen Alemany can provide, for its next phase of profitable growth and shareholder return

Melissa Smith

• Tenure TSR: +63.7% vs. 203.7% for CPAY; 14,000 bps deficit

• WEX’s persistent underperformance (over 3, 5, and 12 years under Ms. Smith’s leadership) indicates that a different operational perspective is needed

• Ms. Smith received just 64.3% support from shareholders at the 2025 Annual Meeting, a decline of 33.4 percentage points from 97.7% the prior year, placing her in the 0.6th percentile of all directors elected at S&P 400 companies in 2024

• Pattern of poor governance until pressured by shareholders (i.e., reluctance to separate Chair and CEO role, poor say on pay votes, and removal of metrics when they no longer “work”)

• Combination of CEO and Chair role has hampered Board oversight of management

Stephen Smith

• Tenure TSR: -22.3% vs. 18.7% for CPAY; 4,100 bps deficit

• Long tenured director and three-year Leadership Development and Compensation Committee Chair who has presided over increasing management compensation as shareholder returns significantly deteriorated

• We question his independence as Leadership Development and Compensation Committee Chair given he is part of close-knit Maine CEO social circle and joined the Board immediately after the CEO and Chair role was combined under Ms. Smith

• Consumer retail experience is not nearly as relevant as public company banking, payments, and health experience brought by Kurt Adams and Ellen Alemany

Sincerely,

Impactive Capital

Source: https://www.sec.gov/Archives/edgar/data/1309108/000092189526000956/ex991dfan14a12236009_041026.pdf