April 30, 2026

Lamb Weston Holdings, Inc.

599 S. Rivershore Lane

Eagle, Idaho, 83616

Attn: Board of Directors

Members of the Board,

Earlier this month, we met with Mike, Jim, and Jan to share our perspectives on Lamb Weston Holdings, Inc.’s (“Lamb Weston” or the “Company”) path forward. We appreciated the opportunity to continue our constructive dialogue and look forward to working together to restore Lamb Weston’s earnings power and premium valuation. As a follow-up to our meeting, we are sharing our presentation with the full Board of Directors (the “Board”) outlining our perspective on the Company’s current position and the actions required to restore earnings growth and credibility.

Lamb Weston is a high-quality business that the market historically rewarded with a premium valuation. Today, however, that premium has been eliminated as prior management’s missteps led to market share losses, declining earnings, and an erosion of investor confidence. While Lamb Weston has made meaningful progress in improving volume trends over the past year, the central issue remains the same:

earnings have not grown and investors lack confidence in the path to normalized earnings and sustainable growth. The Company is at a critical juncture and must clearly articulate a path forward. We believe the appropriate forum to do so is an Investor Day, as it allows the Company to reset the narrative, clearly communicate its path to durable earnings growth, and rebuild investor confidence.

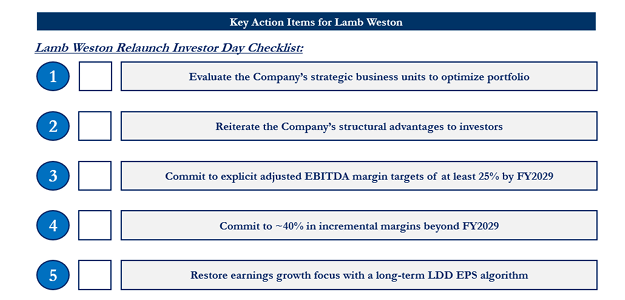

At this Investor Day, the Company must first reestablish the foundation of its story: Lamb Weston is a high-quality business with a leadership position within an attractive industry. We believe the core attributes that historically drove its premium valuation remain intact, including a concentrated industry structure, high barriers to entry, rational competitive behavior, and structural pricing power. While we are confident in this belief, the market is not convinced. It is critical that the Company clearly articulate these strengths not only to restore investor confidence, but also to demonstrate management’s commitment to preserving the fundamentals that underpin its long-term success. As part of this, the Company should also thoughtfully assess its footprint and define which areas are most strategic to its future, aligning capital and resources to support those priorities. Building on this foundation, the Company must then outline a clear path to restoring earnings to a normalized level and, importantly, to driving sustainable growth from there.

The first step is to reset earnings to a normalized level. We believe the Company should attain 25% adjusted EBITDA margins by FY2029 through a balanced mix of profitable revenue growth and cost reductions. As a result of management’s actions over the past year, the Company is now operating within a normalized utilization rate in the low 90s, which should enable a return to stable and balanced pricing environment. Over time, pricing should be supported by low-single-digit volume growth as the Company continues to execute on innovation, commercial, product quality, and supply chain reliability initiatives.

We believe there are meaningful cost reduction opportunities that can help drive the Company toward the FY2029 25% adjusted EBITDA margin target. While the Company’s announced $250 million cost savings program is a starting point, it has been primarily focused on cost of goods sold. We believe a significant opportunity exists within SG&A, which has nearly tripled over the past decade despite only modest volume growth. Addressing this imbalance will require a more rigorous, zero-based approach to cost management. We believe the Company must frame this opportunity through explicit margin targets rather than absolute dollar savings, enabling investors to track tangible progress and underwrite earnings

improvement potential.

Resetting earnings alone is not sufficient. The Company must also demonstrate its ability to deliver sustained long-term earnings growth after earnings are reset to normalized levels. As such, we believe Lamb Weston should clearly articulate a long-term earnings framework, consistent with best-in-class consumer companies. We believe low-single-digit to mid-single-digit revenue growth is achievable and

should establish the foundation of the Company’s long-term earnings growth algorithm. Combined with disciplined incremental adjusted EBITDA margins of approximately 40%, we believe the Company is poised to deliver low-double-digit earnings growth over time, after first achieving 25% EBITDA margins in FY2029.

Most importantly, management must clearly communicate these targets and the benefits of the Company’s position in the industry. Management needs to earn back the trust that they have lost and convince shareholders that the team understands how to maintain a high-quality business and create value. Rebuilding credibility with shareholders will require consistent articulation of strategy, along with disciplined execution.

We believe these actions are both achievable and critical to restore investor confidence and drive longterm value creation. To help maintain focus and ensure accountability, our presentation features a checklist of key actions, which is included below for reference. This checklist highlights the key priorities required to execute this plan and measure progress over time.

We share these perspectives with the goal of supporting the Board and management team in unlocking the Company’s full potential. We look forward to our continued discussions.

Sincerely,

Jeffrey Smith

Managing Member

Starboard Value LP